With import-export turnover equivalent to 2 times of GDP, Vietnam is one of the leading open economies in the world. Therefore, it is understandable that many domestic manufacturing and service industries have been heavily influenced by COVID-19 when facing difficulties related to input and output as well as transportation and logistics.

The Government of Vietnam has asked the banking industry to support affected businesses in various ways: reducing interest rates, extending maturity, and not shifting debt groups to old credit balances. Besides, there is a new loan support package with preferential interest rates from 0.5% - 1.5%.

What can figures say?

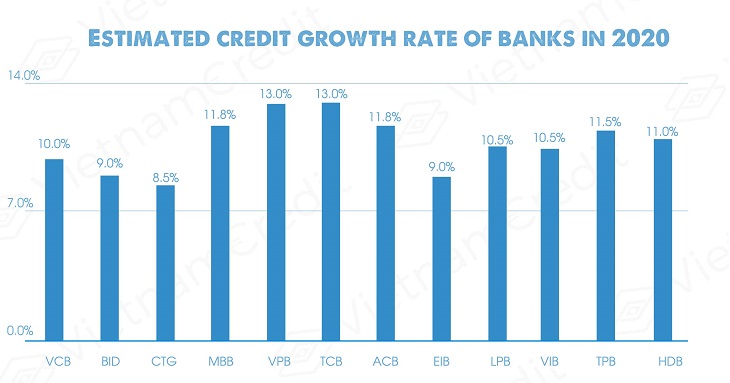

By the end of February, a number of banks had been assigned credit growth targets by the State Bank (SBV) for this year. It should be noted that these are only initial figures, and will be flexibly adjusted by the SBV based on the demand for credit, as well as the aspirations of the banks.

In accordance with the credit growth limits assigned to banks, estimated credit growth of the whole banking industry in 2020 would be about 10%, partly balanced by the impact of COVID-19. The 10% figure is much lower than the planned growth target which was previously set in a conference of the banking industry in 2020.

Reports of banks showed that there is about VND 900,000 billion of outstanding loans (equivalent to 11% of the total outstanding loans) of the affected businesses which may be restructured without changing the debt group.

Therefore, there will not be much influence on the figures on both net interest income or increase in bad debt in the balance sheet, in the context of the fact that the borrowers cannot perform the obligations properly. But it should be noted that there will be about VND 9,000 billion of interest receivable arising in 2020 if the support policies last until the end of the year (with an average interest rate of about 10%).

The credit support package of about VND 250,000 billion, equivalent to 3% of the total credit outstanding of the whole banking industry (or equivalent to about 25% - 30% of newly arising credit balance) will have a direct negative impact on the return on assets (ROA) of the participating banks.

Data from the State Bank of Vietnam showed that credit balance as of the end of February 19 had decreased by 0.28% compared to the end of 2019 and by 0.37% compared to the end of January 2020. This figure is in fact the clearest proof of the effects of COVID-19. So, despite the fact that the credit growth limit of 10% in 2020 has been partially adjusted, it has faced challenges right from the start.

Will there be more difficulties in the next months? There will be more significant challenges for credit growth in 2020. Firstly, the figure will not just be VND 900,000 billion when COVID-19 has continued to spread to other economic partners of Vietnam from Korea and Japan to the EU and US. Secondly, personal and SME credit has been considered a key for growth for most banks over the past few years.

This business segment of banks will probably not be able to recover as soon as the COVID-19 epidemic is over, because of the fact that currently, quite a lot of small and household businesses are pitching their premises on busy business streets in both Ha Noi and Ho Chi Minh City. Finally, can real estate be extended to new credit?

After a letter of help from a large enterprise in the industry, businesses are gradually being supported by removing bottlenecks in some administrative issues. However, it will be difficult for the real estate industry to receive further credit.

At the recent shareholders' meeting in 2020, the chairman of BIDV shared that the credit for the first two months of 2020 has decreased by 2% compared to the same period last year. It is clearly seen that BIDV has suffered significant influence from COVID-19.

Assuming that by the end of February 2020, the total outstanding loans of the whole banking system still decreased (-0.28%), the total outstanding loans of other banks would decrease by about 0.158% in the first 2 months. In particular, there will be some banks (especially private banks) enjoying positive credit growth as they focus strongly on the individual customer segment.

By the end of the first quarter of 2020, it will be quite positive if credit growth reverses to 1%

An important factor of the banking industry that needs special attention is the asset quality which is extremely closely related to the annual provisioning cost, a factor that has a sensitive effect on profits of banks. Basically, the policy of not shifting the debt group is hard to expand in time, because the loans are not guaranteed by the Government.

The quality of bank assets will suffer certain losses, which requires banks to be extremely well prepared. Faced with the fact that not all borrowers will recover after the epidemic, or pessimistically speaking, there will be a large number of bankrupt "debtors", it is necessary for banks to have more flexible observations and assessments with each loan portfolio and corporate bond package.

>> Vietnam’s banking industry 2020

Source: Vietnambiz

")

")

")

")

")

")

")

")

")

")