Since the phone was introduced in 1980 with the main purpose is keeping in touch with people at long distances. As of 2009, mobile phone users worldwide are two-thirds of the population and are becoming more and more popular thanks to technological development. Today, mobile phones are not only a tool for communication but also become the leading utility payment tool which represents a total transaction volume of $250 billion by 2018. This number has increased dramatically worldwide, especially China which is a leading country of online payment that has a mobile payment volume increased twice the time to $5 trillion in 2019 with only two mobile payment apps which are WeChat and Alipay that most of Chinese stores and services are using. Moreover, the emphasis that “payphones are growing rapidly in Mainland China as an outsider, sometimes I find it difficult to complete basic deals without it”. Along with the development of mobile payment is the strength of mobile money which has more effect on the financial market.

Mobile payments are generally defined as the process of the exchange of money for goods and services between two parties using a mobile device, such as mobile phones, wireless devices, computers, or PDAs, in return for goods and services. This definition not include trade without goods and services like exchange money. However, it is not limited to related parties such as Business-to-Business (B2B), Business-to-Consumer (B2C), Consumer-to-Consumer (C2C), or Consumer-to-Business (C2B). And mobile money is “the use of a mobile phone in order to transfer funds between banks or accounts, deposit or withdraw funds, or pay bills. This term is also used for the broader realm of electronic commerce; it can refer to the use of a mobile device to purchase items, whether physical or electronic”. Furthermore, mobile banking is the provision or availing of banking services with the help of mobile devices.

Traditional money has four functions: a store of value, a standard or unit of account, a standard of deferred payment, and a means of payment or exchange. And thanks to having all of the character of money which is a store of value and medium of exchange, mobile money is used more and more like traditional money. Moreover, mobile money also owns the bank’s function which is a safe place to keep or loan money and response demand deposits or checking accounts. Therefore, mobile money is more popular and useful.

In terms of financial market

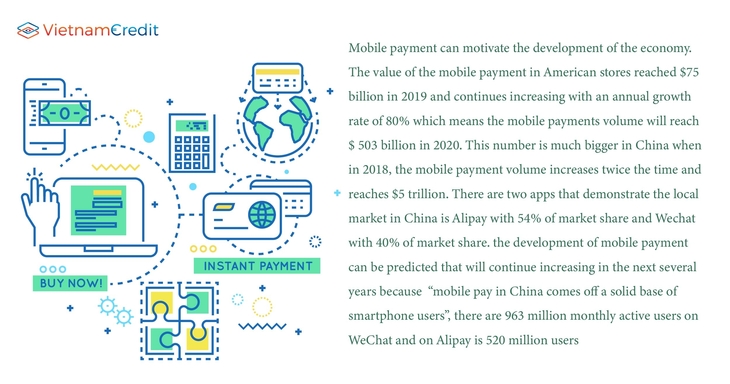

First, mobile payment can motivate the development of the economy. The value of the mobile payment in American stores reached $75 billion in 2019 and continues increasing with an annual growth rate of 80% which means the mobile payments volume will reach $ 503 billion in 2020. This number is much bigger in China when in 2018, the mobile payment volume increases twice the time and reaches $5 trillion. There are two apps that demonstrate the local market in China is Alipay with 54% of market share and Wechat with 40% of market share. the development of mobile payment can be predicted that will continue increasing in the next several years because “mobile pay in China comes off a solid base of smartphone users”, there are 963 million monthly active users on WeChat and on Alipay is 520 million users

Second, mobile payment can enhance commerce. It means that shoppers spend more by using mobile payments. Thank to having the function of the bank, mobile payment can provide security that cash does not have, and it can replace the credit or debit cards for unbanked. Additionally, it is much easier to pay goods and services by using a mobile phone compare with going to the bank. Furthermore, the app is connected with the online money market fund Yu'e bao which encourages users to fund and spend money with Alipay. Interest rate is also an interesting factor that makes the online money market - Yu’e bao become the largest money market fund in the world with $2.17billion. In addition to Alipay, the electronic payments volume of research investment company CLSA will reach 300 trillion yuan in 2021. In addition, American consumers care not only with interest rates but also with accessing loyalty program points and rewards through their mobile wallets. There are 57 % adult care in these programs. And he also cited the identity from P.J. Ritters who is a director in the retail and consumer practice at PwC that these types of benefits could get consumers to spend more, especially the buyer data is leveraged to send relevant promotions based on things like their purchase history. Retailers can also be reached by narrowing the gap between the Web and real store shopping, making it easier for consumers to purchase.

In terms of customers

The mobile payment allows customers to pay quickly and easily, even if you do not carry cash or a card. In China, altering asking “Do you take credit cards?” in the stores, the question will be "Do you take Alipay? WeChat Pay?" and most of the business activities has the appearance of mobile payment. There are 2 main reasons that allow china to the leader of mobile payment which is a solid base of smartphone users and a less developed financial system. Moreover, consumers just keep their smartphones close to point of sales (POS) terminals and pay instantly. Unlike card transactions, the expiration date or security code on the card is not needing to verify - all stored on the customer's mobile device. So, it makes the transaction faster and customers can save time and money because they do not have to go far or rely on the courier or other means to receive their money for their family. Furthermore, by using mobile payments, consumers no longer have to take cash-related security risks or worry whether they have enough cash in their physical wallet to pay for mobile payments to reduce the risk of cashing theft. Moreover, mobile payments are a safe way to pay. Credit card information is stored on the cloud, not on a smartphone. In this way, iTunes has the largest credit card database in the world.

In terms of business

Mobile payment can remove the limit about geography therefore, it allows owner stores to expand their market and help them transact with customers outside their stores such as trade shows, local expo even in foreign countries. Moreover, when the owner uses mobile payment as the main payment method, it can help them save money because they have to pay monthly fees and transaction fees if they receive a credit card from a bank. Furthermore, thanks to the convenience of mobile payment, the returning customer’s rate will increase. The bank also gets a benefit from the mobile payment. The bank has a big opportunity to “cut cost, increase efficiency, and expand the customer bases”. When the bank develops the mobile banking system, the system can help the banks be smaller by cutting down some brand bank, which leads to saving millions in operational expenses.

Mobile payments are being developed and improved by many private businesses and mobile operators because they look at the potential market for this service. With many benefits of mobile payment for customers, more and more people prefer using mobile payment rather than using banks’ services. The quick development of mobile money can harm the current bank’s system like the credit or debit card system in which the bank generates fees from both card users and retailers accept them. For example, in the US, the bank could lose two to three percent of the latter fees which monopoly provided and control by the bank. Therefore, the change is necessary for banking at this time to avoid losing the market. There are several challenges that are easy to see when the banks enjoy this market.

Competition

In the US, banks are in danger of losing the retail payment market because traditional bank payment services are competing fiercely with startups such as Paypal, Google, and Apple because they are providing mobile payment services. As a consequence, most major US banks are struggling to improve and develop their mobile banking platform.

Customers’ behavior

Changing customers’ behavior has never been easy before. There are 95% of mobile banking users access internet banks to check their balance, transaction history, or mobile check transactions. Moreover, in some developed countries like The US, mobile payment still has a high barrier with consumers. Many people remain using traditional payment methods and gainst new habits. There are only 20% of customers of 54% banks per 89% banks who provide mobile banks resign to use bank’s services and having a small group is actively using these services that most users are younger consumers. However, the bank must continue to develop and expand this project because customers can move away when telecoms and private enterprises can provide them with a similar service, even better with more incentives. The most common reason that banks provide mobile banking services is to ‘retain existing customers’ with 29% of the bank in the USA, competitive pressure is a second important for offering mobile banking with 24%, only 23% of banks offer mobile banking to attract new customers. And 21% of banks which seem to be large organizations provide this service as a market leader of technology.

Market disruptions and financial instability

Mobile payments can create financial instability and volatility on the market. Therefore, banks need to understand and accurately predict both positive and positive effects of mobile payment services.

Moreover, when the policy has not responded to the rapid change of the market, many non-bank companies and organizations can provide detailed information to regulators and financial institutions to make Decisions benefit them rather than the interests of the entire financial market.

● Will banks ever be successful in Mobile Payments?

Thanks to mobile financial services, millions of poor people can access financial inclusions who cannot have access to the bank by traditional methods. In many parts of Africa, there is simply no bank infrastructure, so people cannot go to the bank in the traditional way. Therefore, mobile payment represents the full effectiveness of its in areas of financial difficulty and infrastructure. So, with their business rules, can bank demonstrate the mobile payments. To know if the bank has a successful mobile payment business, accessibility assessment is the most accurate way possible. To ensure access to and fulfillment of the requirements for community members, the bank needs a sufficiently wide network of branches. However, the costs for the establishment of affiliates are so large that it will be difficult for many banks. On the other hand, mobile payments allow users to operate continuously at every time and everywhere that they want. With unlimited geographical features, mobile payments once again prove their superiority over mobile banking. In addition, most countries have reduced MNO regulations while banks are subject to strict regulations by central banks and the respective deposit protection authorities. Therefore, it is hard for mobile banking to beat mobile money from MNO.

Complied by Vietnam Credit

")

")

")

")

")

")

")

")

")