Credit score is a very important factor for banks to consider approving loans and issuing credit cards for their customers. However, not many people have enough knowledge about this.

Credit score is normally used by financial institutions to assess a person's creditworthiness who is using or going to use their lending facilities. The higher one’s score, the better he/she will be appreciated. The 740 score is considered to be excellent and it will help people get a good interest rate when dealing with banks.

• Credit score determines the customer's ability to borrow as well as the credit limit that the bank can disburse when their customer has a need for a loan.

• Credit score affects customers' subsequent loans if the credit score is lower than the minimum level that the bank can offer.

Credit score is usually calculated based on the following factors:

This reflects whether a person pays on time, pays off the debt, or pays late. Most credit scores are assessed based on the borrower's payment history. Serious and timely repayment will be the most important factor affecting an individual's credit score.

Reflecting all debts, the credit debt ratio is made up of the total amount of loans granted to a person by the bank. According to experts, people with the ideal score tend to maintain the credit debt ratio at an average of about 7%.

This reflects the period of time when a person's credit account is opened. This time should be as long as possible because the bank or credit institution can assess one’s financial behavior in a holistic and more complete way.

Opening new credits is often unpopular, especially for a short time. That one’s credit stays open for at least 6 months will boost their credit score and help them build a long and solid credit history.

This reflects all the types of credit one may have such as: Credit cards, loans (tuition loans, home loans, car loans ...) Experts say that having used a lot of financial leverage and paid due debt shows that the borrower is able to handle credit debts well.

Credit score is an indicator of one’s current financial position, with which a bank can decide whether or not to grant them a loan. In many other countries, credit institutions rate a borrower with a FICO credit score (Fair Issac Coporation - a very reputable personal credit rating company) on a scale of 550 – 840. In Vietnam, however, things are run in a distinct way. Experts have set up a separate credit score system with a slightly different scale and under the management of the Credit Information Center (CIC). To have better understand about this system and its importance, please refer to our personal credit scoring system.

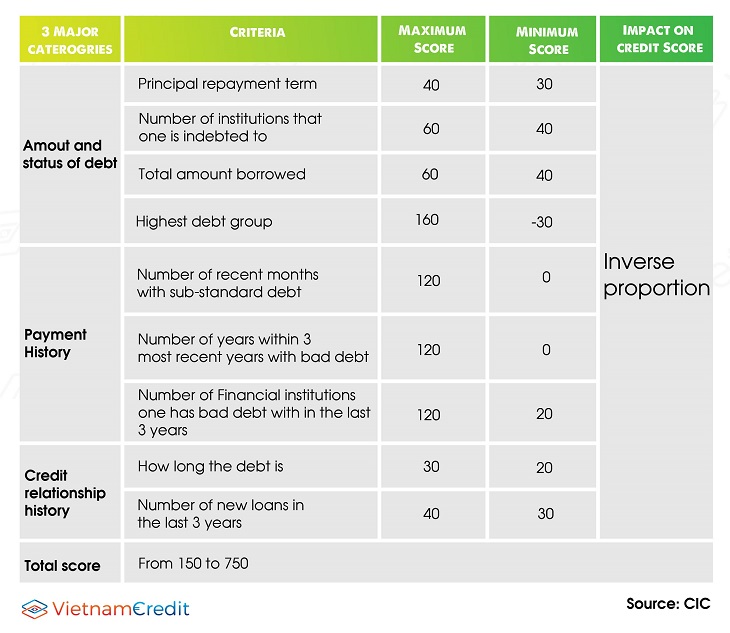

There are 3 major categories that affect one’s credit score: Amount and status of debt; Payment history and Credit relationship history. Specialists will calculate the credit score based on these 3 factors. Details of the formula are shown in the following table:

It is obviously understood that the lower one credit score is, the higher the interest rate they will have to pay. If the score is too low, one is not even considered qualified for a loan. Therefore, if you want to get bank loans at a lower interest rate than others, find ways to improve your credit score.

It is no doubt true that many borrowers are interested in credit scores and are looking for secrets to improving their financial reputation. Using credit cards effectively is said to be one of the leading solutions to increase the credit score, helping save a relatively large interest in the future. However, there still exist many other ways that not many people have found out. VietnamCredit experts have come up with a number of techniques to help you improve your credit score.

Alice Hoang Thao - VietnamCredit

.")

")

")

")

")

")

")

")

")

")