With a huge data sources, VietnamCredit's experienced experts conducted Vietnam Insurance Industry Report based on scientific and objective principles. The report gives customers important information related to Vietnam's insurance industry including overview about the industry, legal regulations on insurance, types of insurance, what is happening in Vietnam’s insurance market, and industry forecast.

Insurance companies are evaluated and ranked based on their capital size, gross written premium, market share, claim payment, total assets, reverse, investment, etc. and objective judgments of VietnamCredit’s experts.

Currently, there are 66 insurance companies in Vietnam, of which 30 are non-life insurers, 18 are life insurers, 2 are re-insurers, 16 are insurance brokers and 21 are representatives of foreign insurers.

2019 marked the sixth year in a row when Vietnam’s insurance market had achieved a premium growth rate of over 20%. Total assets were recorded VND 454 trillion, an increase of 15.03%. Household incomes are growing in accordance with people’s awareness of the benefits that insurance would bring. In addition, major insurers have been granted access to capital and are introducing innovative and appropriate products through multiple distribution channels whilst regulators have made efforts to improve the transparency and standards. Therefore, premiums are forecasted to experience a double-digit growth in the not-so-far future.

However, there also exist several challenges for participants in this promising market. Access to capital is almost available for “giants” while the opposite is true for many domestic non-life companies. Moreover, most of Vietnamese households still do not have sufficient income to purchase life insurance, and the economy remains undiversified, limiting the growth potential of lines such as credit or financial guarantee and general liability insurance.

On top of that, current growth rate is likely to slow. High inflation rate may affect buyers’ perspective on the value of insurance products. Besides, natural disasters are always lurking in this tropical country. The expansion of the government’s mandatory health insurance program is also among major threats to insurers in Vietnam.

In 2019, life insurance premium in Vietnam reached VND 107.79 trillion (~ USD 4.66 billion), up 23% year-on-year. Total assets of this segment increased by 17.23%, to VND 364,932 billion. Total reserves followed the upward trend and reached VND279,976 billion, rising 18% compared to the year 2018.

The growth in life insurance premiums in Vietnam is supported by some structural factors, including: a young population, urbanization and the growth of the middle class, the absence of a comprehensive social security system, high saving rates compared to the number of high-income households, diversified products, etc. The Vietnam Ministry of Finance aims to raise the total population who possess life insurance from the current level of nearly 8.5% to 11% in 2020, and to 15% in 2025.

There are 18 life insurance companies with more than one thousand representative offices and general insurers. Despite the significant growth rate of premium, half of the insurers on the market suffered from losses.

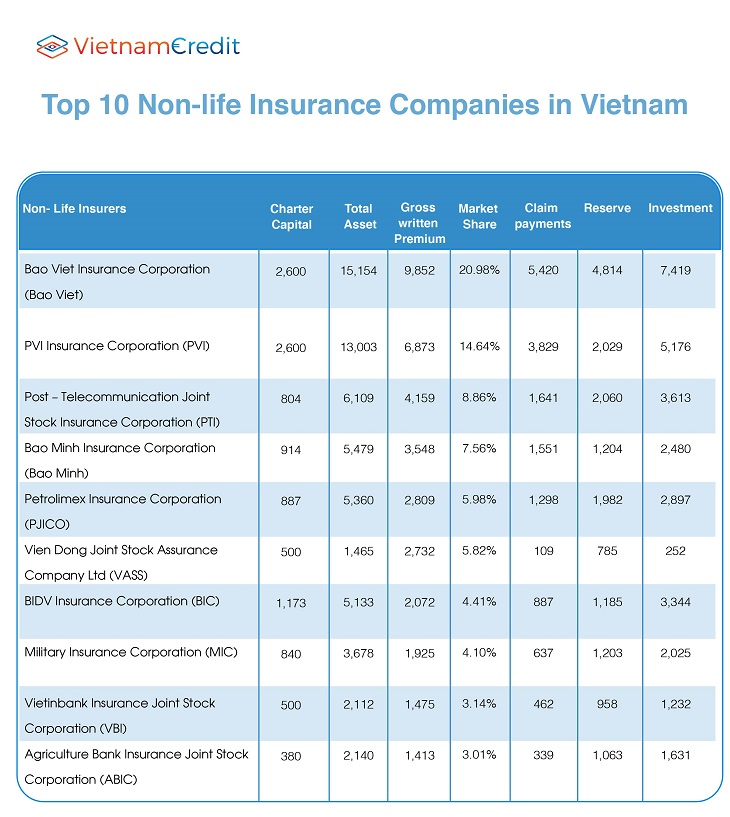

Non-life insurance segment in Vietnam also witnessed a positive growth of 11.6% in premiums revenue which reached VND 52,380 billion (~ USD 2.26 million) at the end of 2019. Total assets of non-life insurers went up by 7.89% to VND 89,447 billion.

The market of non-life insurance is smaller than that of life insurance, and dominated by domestic firms – Bao Viet and PVI. The total number of non-life insurers is nearly double that of life insurers, increasing the competitiveness.

Health and personal accident insurance along with motor vehicle insurance comprise the largest areas of premium revenues. Rising income levels plus the ASEAN FTA in 2018 are likely to promote domestic passenger car demand with an expectation of 20% growth in 2020 vehicle sales revenue. As basic car insurance is compulsory in Vietnam, this should reflect an expansion of non-life insurance in the coming years.

According to Boston Consulting Group, the number of middle-class people in Vietnam will be 33 million in 2020. Changes in the awareness of middle-class individuals about protection and insurance will promote the growth of Bancassurance – the selling of insurance products and services by banking institutions.

This is a key opportunity for financial institutions, as the Bancassurance market in Vietnam is underdeveloped in comparison with other countries. Expanding customer needs, increasing demand for life coverage and the growing need for medical protection and long-term savings for education and retirement all offer ample opportunities for players to provide a diverse and sophisticated range of market-leading life insurance solutions. The partnership with banks in delivering this product is, and will continue to be a significant trend.

In 2019, insurance premiums revenue through Bancassurance took over 30% of total revenue, doubling compared to 2017. 2019 saw an increase in the Bancassurance trend after a lot of major deals had been signed. The famous business deal between FDW and Vietcombank for an estimated USD 400 million signified a major trend for Vietnam’s Bancassurance segment, helping it to catch up with the rate of 70% in developed countries. More and more banks consider this channel a strategic development for both a stable income stream and diversification in satisfying customer demand.

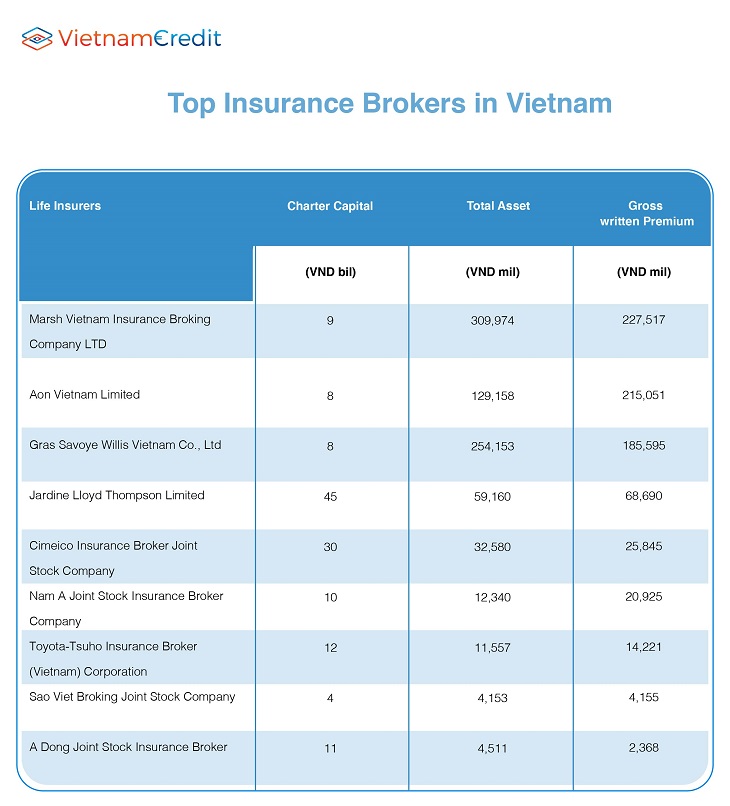

The Insurance Broker market is still dominated by the four foreign invested companies including Marsh, Aon, Gras Savoye Willis and Jardine Lloyd Thompson, which account for 95.7% of total premiums arranged by brokerages. Other brokers only have a small revenue of 4.93% of total premiums.

Two Vietnamese players in Vietnam’s re-insurance market are PVIRe and Vinare. Both saw a significant growth in premiums revenue, however, their future profits are expected to remain the same.

")

")

")

")

")

")

")

")

")

")