The "Big 4" group is still leading in absolute value, but the group of private commercial banks is the speed locomotive.

In banking activities, profit is often the first and outstanding criterion when comparing among members. However, from the perspective of executive management and following the long-term strategy, total assets are the fiercely tacit competition factor.

"Profit is transient, market share is forever" - this view has been discussed by some

commercial bank leaders before. Profits in many cases witnessed ups and downs through stages, but the requirements for total assets must always follow the pace of development and expansion of the market and the economy. It is a long way.

The total assets of each commercial bank are the same as a country's GDP. It includes and reflects all values of each bank, of which the most important customer and market share.

Banks may lose or reduce short-term profits, but if they lose market share and customers (reduce total assets), a step back can have long-term effects.

BizLIVE reviews the evolution of total assets of commercial banks in the first 9 months of this year, as well as important indicators of the market share of deposits and loans, etc.

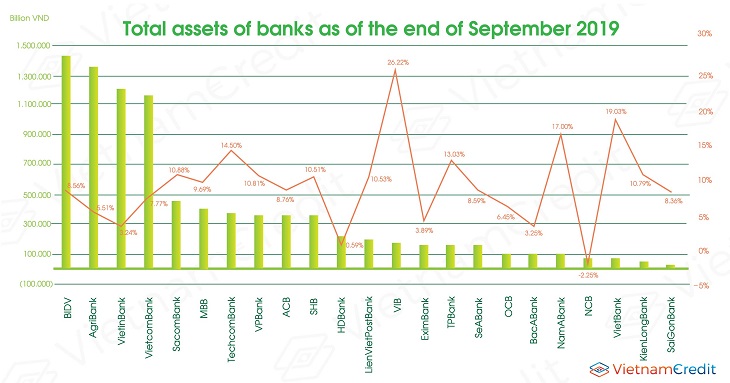

Figures of 24 banks' financial statements for the third quarter of 2019 showed that, by the end of September 2019, the total assets of this group had reached VND 8,175 million billion, up 8.9% compared to the beginning of the year. In particular, the group

"Big 4" banks with state capital (including BIDV, Agribank, VietinBank, and Vietcombank) are still leading, with the total assets of each bank has exceeded 1 million billion.

In particular, BIDV and Agribank have reached this milestone since 2016; VietinBank in 2017 and Vietcombank in 2018.

Specifically, with total assets of VND 1,425 million, an increase of 8.56% compared to the beginning of the year,

BIDV is the bank with the largest total assets of the system.

Agribank has not yet released the

financial statements for the third quarter of 2019, but according to the updated figures by the end of June 2019, the total assets of the bank reached VND 1,353 million, up 5.51% compared to the beginning of the year and ranked second in the system.

If any bank wants to surpass BIDV, in the third quarter of 2019 alone, the bank's assets will have to grow by more than 5.63%.

With the asset size of VND 1,202 million as of the end of September 2019, VietinBank is ranked third in the system but the bank has the slowest asset growth rate in the group, with an increase of only 3.24% compared to the beginning of the year.

Vietcombank ranked 4th in the system in terms of total assets, with the achievement of VND 1,157 million, up 7.77% compared to the beginning of the year.

Accordingly, the total assets of these 4 banks alone reached 5,138 million VND, accounting for 63% of the total assets of the survey team.

In the group of joint-stock commercial banks, SCB is the bank with the largest total assets with 552.5 trillion dongs, up 8.57% compared to the beginning of the year.

Next are other banks such as Sacombank (VND 450.2 trillion), MBB (VND 397.4 trillion), Techcombank (VND 367.5 trillion), VPBank (VND 358.2 trillion), etc.

In terms of growth, VIB is the bank with the fastest growing total assets in the first 9 months, with a growth of 26.2% to 175.6 trillion dongs. Similarly, some other small and medium-sized banks such as Vietbank, NamABank, and Tpbank also had good asset growth, with an increase of 19%, 17%, and 13% compared to the beginning of the year.

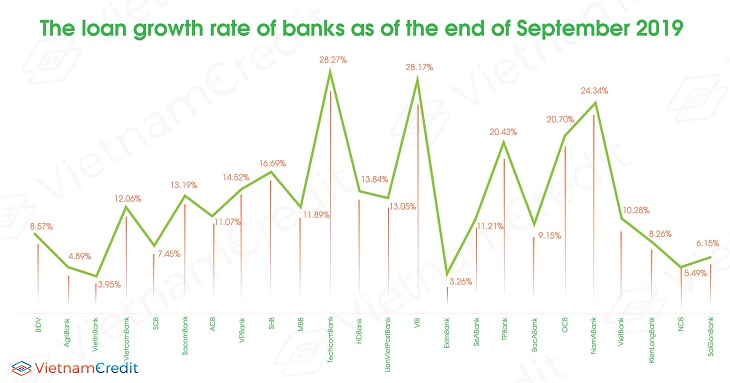

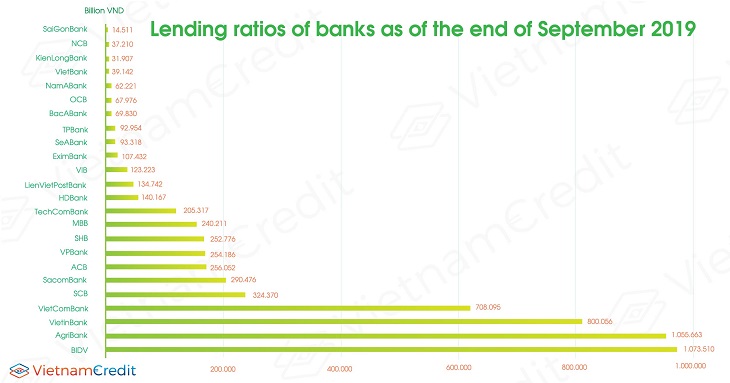

In terms of customer loans, as of the end of September 2019, BIDV continued to lead the system while spending 75.3% of its total assets, equivalent to more than VND 1,073 million billion loans to the economy, up 8.57% compared to the beginning of the year.

By the end of June, Agribank also spent 1,055 million dongs on customer loans, up 4.89% compared to the beginning of the year.

VietinBank and Vietcombank are offering loans of VND 899 trillion and VND 708 trillion respectively, up 3.95% and 12% compared to the beginning of the year.

Meanwhile, the group of joint-stock commercial banks, though having a smaller market share, is the group with much faster loan growth. Techcombank and VIB are two typical cases.

In the first 9 months, customer loans of Techcombank and VIB grew by over 28% compared to the beginning of the year. This figure at NamABank is 24.34% and at OCB is 20.7%. It is known that, except NamABank, the three remaining joint-stock commercial banks were soon approved by the State Bank to apply Basel II standards, accordingly, it is likely that the operator has raised the "room" for credit.

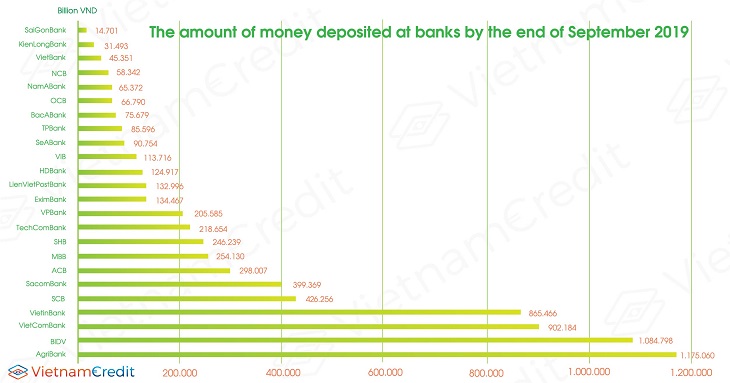

At the target of customer deposits, only by the end of June 2019, the amount of money deposited into Agribank reached VND 1,175 million, surpassing the figure at the end of September of BIDV of more than VND 1,084 million.

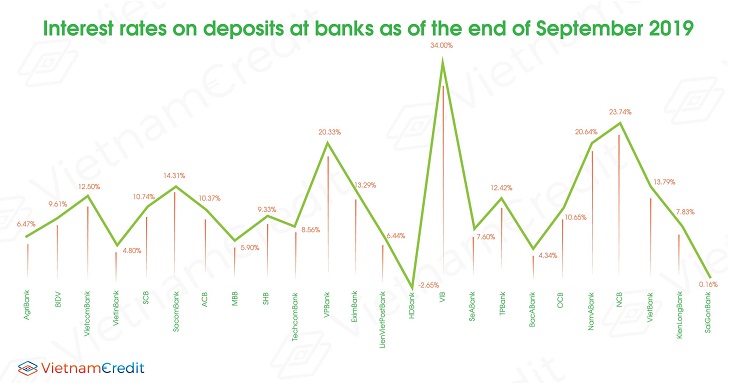

VIB continues to be the bank with the fastest rate of attracting customer deposits by increasing 34% in 9 months, followed by NCB (23.74%), NamABank (20.64%) and VPBank (20.33%).

Source: CafeF

")

")

")

")

")

")

")

")

")

")