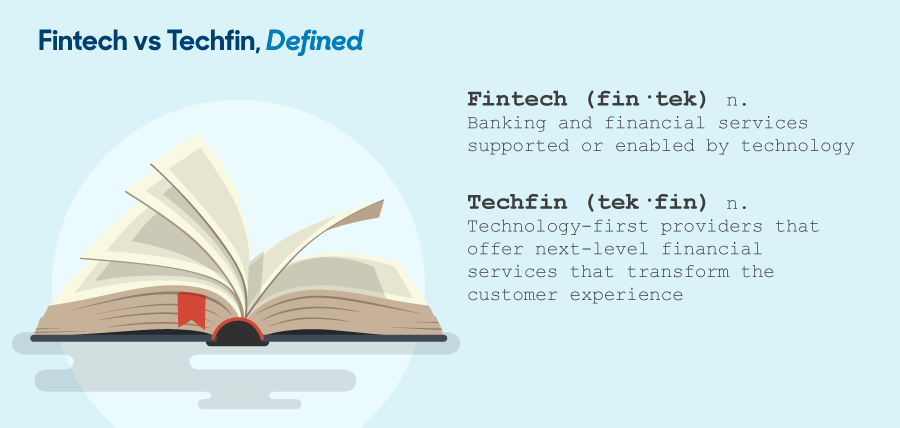

The main difference between fintech and techfin is based on the origin of organization. Fintech is a term which is used to refer to an organization that provides financial services through digital technology to reduce costs, increase revenue, and remove barriers.

For instance, the basic product of fintech is online banking, which is provided by most traditional banks. Non-traditional financial services are more popular such as PayPal, Zelle and Venmo in the US, or online banks like Starling, Monzo and Revolut in the UK.

Meanwhile, techfin is usually used to refer to technology firms that offer financial products to expand services such as Google, Amazon, Facebook and Apple in the US, or in China with Baidu, Alibaba and Tencent.

A few years ago, Jack Ma, Co-founder and CEO of Alibaba Group, described the difference between fintech and techfin: " There are two big opportunities in the future financial industry. One is online banking, where all the financial institutions go online; the other is internet finance, which is purely led by outsiders."

Fintech or Techfin

According to World Fintech Report 2018 from Capgemini, LinkedIn and Efma, most of successful fintech firms are focusing on narrow markets, or segments where traditional financial institutions fail, but they struggle to achieve growth. Meanwhile, traditional financial institutions, having large customer bases and abundant capital, are stifled by traditional systems.

In both cases, the success of the organization will depend on the ability to collect, analyse huge blocks of data, learn from customer data to improve personalization and interactivity in real time, and expand the service to meet the needs of consumers.

Years pass, the financial institutions and fintech firms have finally figured out that symbiotic relationship is the best solution for long-term development.

The cooperation of banks and fintech firms can bring strength to both sides, creating a stronger entity than a single existence. The great advantage of fintech organizations is their innovative thinking, flexibility, "customer focused" perspective and dedicated digital infrastructure. These are the advantages most traditional financial institutions do not have. At the same time, most banking institutions have greater scale, brand awareness and reliability. They also have the capital, legal knowledge and available distribution network.

The challenge is to create a favourable environment, to promote cooperation and to avoid restraining the above characteristics of the two.

The traditional financial institutions are still competing with techfin “giants” in the future banking ecosystem though their cooperation is well running. According to Bain company, many technology giants have success factors: digital application capacity, large customer database, proficiency in improving customer experience, and enough autonomy to expand the brand to the banking industry. Of more concern, some of these fintech firms have built a high credibility, which previously belonged only to traditional banks and credit institutions.

As a result, more and more consumers are ready to use financial services from non-traditional financial institutions, especially if the service offers a superior experience than traditional institutions. The ability to shift revenue streams from other sectors (such as retail) to the banking and finance industry can completely change the balance of competition.

It is expected that the demand for products and services of fintech firms and large technology companies will increase, as many consumers are familiar with modern digital services. This is especially true for younger, older consumers with the same digital devices.

“Techfin firms start with technology and wonder how that can be used for commerce and trade. Alternatively, fintech firms start with existing trade structures and wonder how to make them cheaper and faster with technology. I liken it to fintech firms are making faster horses whereas techfin firms are working with airplanes” shared Chris Skinner, Advanced product development engineer at ADAC Automotive.

More and more, people will get irritated when they’re forced by bank policies and processes to use non-digital channels for daily financial transactions. Traditional banking organizations cannot rely on providing checking accounts and loans only. Competitors are already accounting the most for significant parts of the banking value chain with the potential of limiting banks to becoming nothing more than utilities.

As financial and technology organizations embrace a broader view of banking, offering both banking and non-banking services, the ultimate winner will be the consumer regardless of which provider they select.

The future of the banking industry will depend on its ability to leverage the power of customer insight, advanced analytics and digital technology to provide services that help today’s tech-savvy customers manage their finances and better manage their daily lives.

Source: forbesvietnam.com.vn

")

")

")

")

")

")

")

")

")

")