Before making the decision to lend money, there are a few factors which you should consider to make sure the borrowers have the ability to pay the money back.

It is important to perform risk management by gaining as much information about the subjects as you can, but amidst a vast amount of information, it might take you quite some time to analyze and decide on which ones are most important. In this article,

VietnamCredit presents to you some of what we thought to be the most important factors to consider before deciding on loaning the money to a business.

I. Purpose of the loan

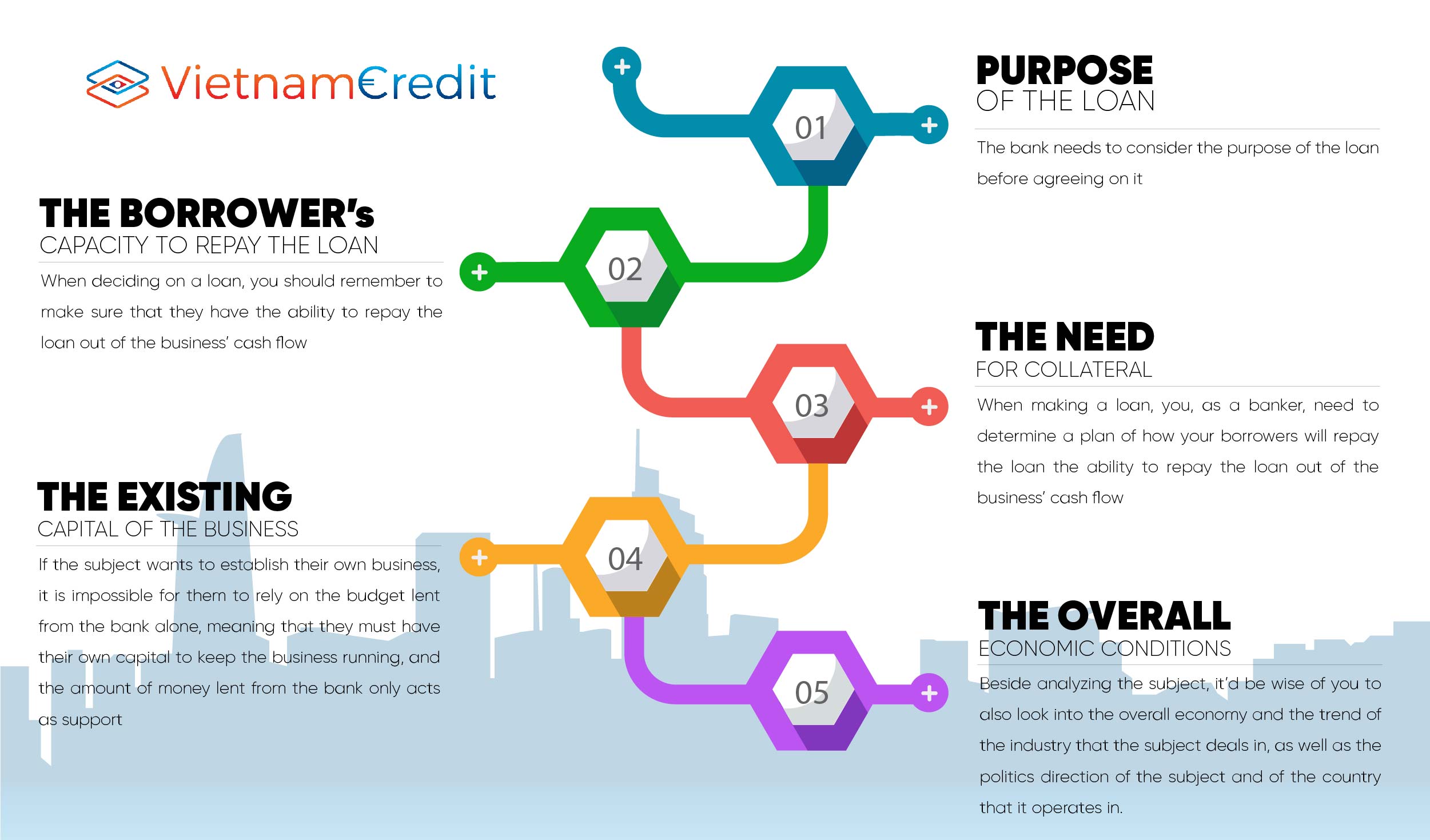

Firstly, the bank needs to consider the purpose of the loan before agreeing on it. If you are a banker, you need to learn about what the loan is going to be used for, by which portion, the solidity of the business, and their record of performance to decide on the risk level and the chance of success or of bankruptcy of the business. You also need to learn the specific amount of money the borrowers need, and what is their plan of paying for the debt.

In order to make a better informed decision on this matter, you could require the borrowers to provide you with a business plan, including: summary of the business and what it offers consumers, how experienced the management team is, how the situation of the competitive environment is, what the target market is, and a financial statement.

After receiving the business plan, then you could get it analyzed and evaluated based on the five Cs, including character, collateral, capacity, capital, and conditions. After all these processes, you might be confident enough to decide on whether to loan the business or the individual the money or not, but if not, you can still ask for more information regarding their operation.

II. The borrowers’ capacity to repay the loan

When deciding on a loan, you should remember to make sure that they have the ability to repay the loan out of the business’ cash flow. You can determine this by tracking and analyzing the financial situation, the ratio between the debts and the income of the business, as well as the amount of free cash flow that the business own. These informations will provide you with better knowledge regarding the subject, thus aiding you in making the lending decision in hope of getting the loan repaid in the future.

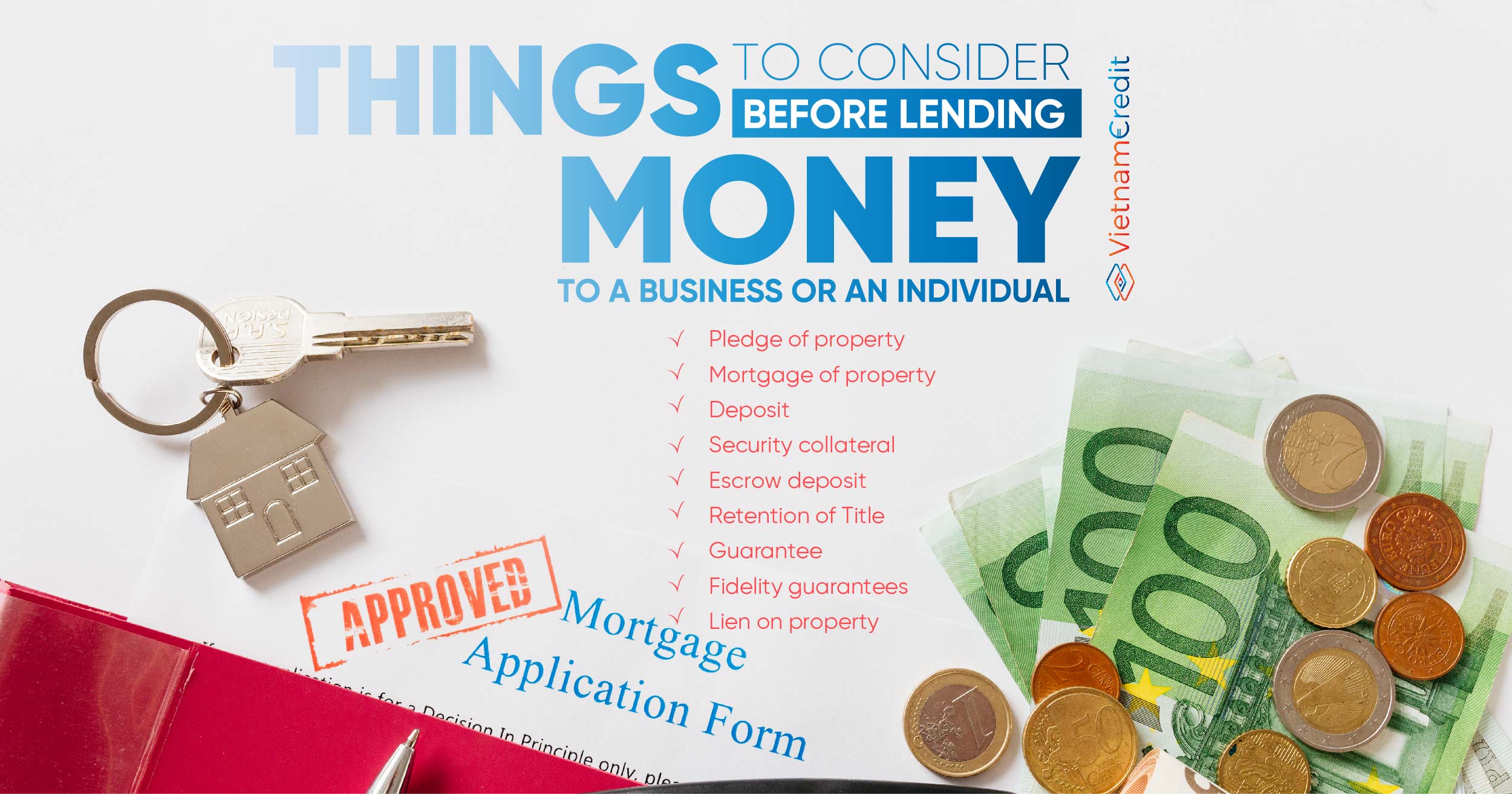

III. The need for collateral

When making a loan, you, as a banker, need to determine a plan of how your borrowers will repay the loan. In the Vietnamese civil code there are 9 guarantee methods, including: Pledge of property; mortgage of property; deposit; security collateral; escrow deposit; retention of Title; guarantee; fidelity guarantees; lien on property, in which the collateral method is only the last resort in case the business of your borrower fails. However, in the Vietnamese business world, this method is considered to be a compulsory and the most important. If the borrower default on the loans, then you will have to fall back on the collateral, and if you don’t consider it carefully, the sale of the collateral may not be enough to pay off the loan.

Some good examples of collateral may include, but not limited to, property or assets, as they can be sold for a fairly good price if the borrowers fail to pay as planned.

IV. The existing capital of the business

If the subject wants to establish their own business, it is impossible for them to rely on the budget lent from the bank alone, meaning that they must have their own capital to keep the business running, and the amount of money lent from the bank only acts as support. Therefore, you must also research on the invested capital of the business to make sure that the borrowers invest something in their business, proving that they have confident in its success, and in case it fails the business may actually lose something. If even the owner does not invest in his/her own business, why should the bank?

Collecting the aforementioned information may not be easy due to the vast amount of them, and if you are not professional, it is quite likely that you might miss the important information, affecting your decision. This is why you can rely on Vietnam Credit. With our

Company Report, consisting of the latest and most detailed information regarding your subject, conducted by our finest and most experienced experts, we are confident that our service will aid you in making the most informed, fastest and best decisions.

V. The overall economic conditions

Beside analyzing the subject, it’d be wise of you to also look into the overall economy and the trend of the industry that the subject deals in, as well as the politics direction of the subject and of the country that it operates in. Doing this means you are taking other factors that the business managers might not be able to control and might affect the business performance, thus granting yourself the ability to prevent the defaults caused by these factors. This could be considered a form of risk management on it own.

In this case, you may also make use of the

Industry Report provided by Vietnam Credit. We provide you with the latest developing trend, as well as the financial information regarding the industry, providing you with the ability to evaluate whether to make the loan or not.

VI. Conclusion

In conclusion, in order to prevent the risk of losing money in case your borrowers fail or go bankrupt, it is important for you to gather their business information, as well as performing risk management by considering the aforementioned factors in addition to other factors. You may choose to do it on you own, or you could rely on the services provided by Vietnam Credit, as we can provide you with all the business information you require, as well as the credit level of your subject. Moreover, in case your loan turns into a bad debt, we also have a debt collecting service to help you, so you can be totally confident in relying on us.

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")