Bad debt balances at many banks increased sharply in the first quarter of the year, making the NPL ratio reach above the threshold of 3%. At some banks, this ratio was even at double digits.

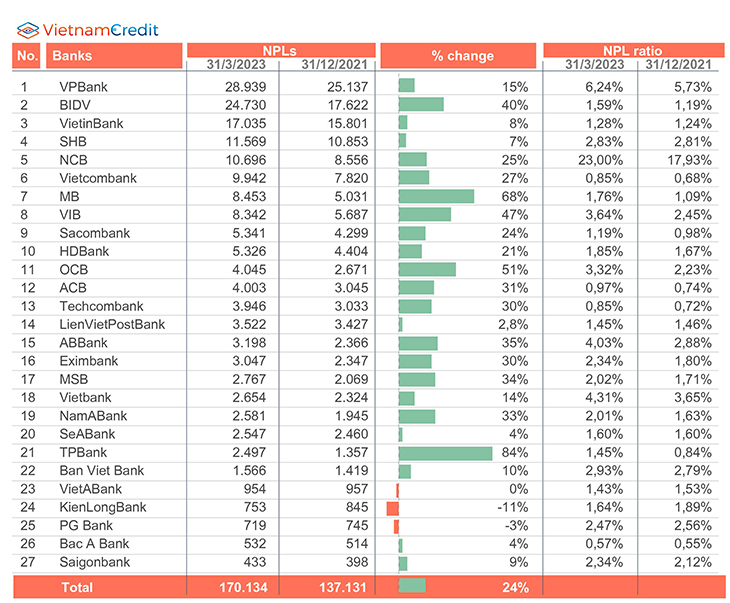

According to statistics from 28 banks that have published financial statements, as of March 31, 2023, bad debt balance increased by 24% compared to the beginning of the year, to over VND 170,134 billion. Moreover, nearly 90% of them recorded an increase in bad debt. The NPL ratio at many banks exceeded 3% such as NCB, VPBank, Vietbank, ABBank, VIB.

VPBank is the bank with the highest debt balance in groups 3 to 5 in the first quarter of 2023 with VND 28,939 billion. The majority of bad debt continued to come from consumer finance company FE Credit as the parent bank's bad debt as of March 31 was just over VND 13,500 billion.

Following VPBank is BIDV with bad debt reaching VND 24,730 billion, up 40% compared to the end of last year. In particular, group 3 debt (substandard debt) increased by 127%; group 4 debt (doubtful debt) increased by 59% and group 5 debt (potential loss of capital) increased by 13%. However, the ratio of NPL to total loans of BIDV is still below 2% (1.59%).

Some banks had bad debt balances increased rapidly in the first quarter such as TPBank (up 84%), MB (up 68%); OCB (up 51%); BIDV (up 40%).

Sharing about the increase in NPLs at the recent annual general meeting of shareholders, banks’ leaders all said that the main reason was due to the fact that the economy was under a lot of pressure from the outside, weakening the resilience of businesses.

The economy in general tends to decline, negatively affecting customers' business results. Especially negative impacts from the real estate market, corporate bond market, rising interest rates, and tight credit have caused some debts to be grouped as group 3 to 5 debts.

In addition, the expiration of Circular 14 on debt restructuring, debt group retention, and interest rate exemption and reduction for customers affected by the COVID-19 epidemic also puts pressure on customers.

Analysts say that the banking sector's bad debt risk this year is heavily influenced by risks from restructuring debts, the quiet of the real estate market and corporate bonds.

NPLs at VPBank mainly come from the consumer finance segment. Sharing at the 2023 annual general meeting of shareholders, General Director Nguyen Duc Vinh said that 2022 was a very difficult year for consumer finance companies and that would continue in 2023.

The consumer credit segment is characterized as posing high risk yet high return and is directly affected by fluctuations in the economy. However, VPBank's management board still considers this to be a very potential market. The bank has approved the restructuring plan of FE Credit and will implement it in the near future.

Regarding bad debts at the parent bank, Mr. Vinh said that the NPL ratio of the bank in the first quarter increased sharply and is expected to continue to increase in the second quarter, then gradually decrease in the last two quarters of the year to about 2.2%.

Explaining its large bad debts, NCB said that in addition to the general reasons mentioned above, the bank has reclassified bad debts and overdue debts in accordance with the status of debts according to regulations of the State Bank (SBV).

The recent official issuance of Circular No. 02 by the State Bank of Vietnam on rescheduling the debt repayment term and keeping the debt group unchanged (effective until June 30, 2024) is one of the solutions to support both businesses and banks in the current difficult context.

Dr. Can Van Luc, Chief Economist of BIDV, member of the National Monetary and Financial Policy Advisory Council, said that this is a firm decision, which is expected to help prevent an increase in bad debt on the balance sheet, allow access to capital of businesses, borrowers, and support liquidity in 2023.

However, Mr. Luc also noted, if businesses do not recover, the risk of bad debt may be greater, negatively affecting both businesses, borrowers and financial institutions.

According to SSI Securities, with Circular 02, borrowers will have more time to fulfill their debt obligations while waiting for the economy to fully recover at an appropriate time.

In addition, banks will ease the pressure on both balance sheet and income statement as the risk of increased bad debt ratio will be carried over to the second half of 2024. Profit pressure also eases from 2023 until the second half of 2024 when bad debts will more obviously reflect borrowers' situations.

Source: vietnambiz

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")