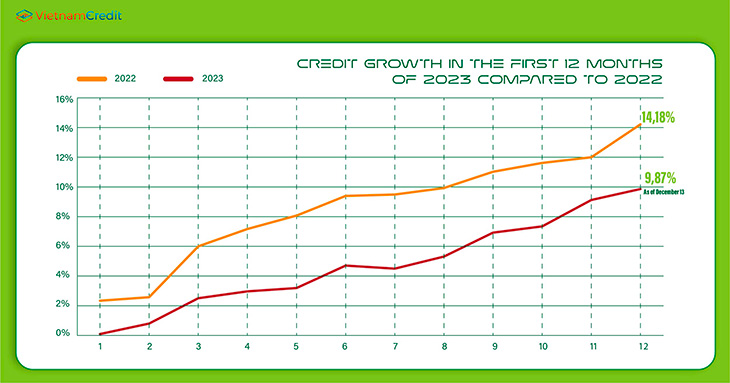

In a difficult economic context and weak capital absorption capacity, credit growth has had a slow start since the beginning of the year. In July, the credit growth rate only reached 4.56%, lower than the figure at the end of June.

Credit increased more positively in the following months and especially in the past three months. According to the latest data from the State Bank (SBV), as of December 13, credit growth across the economy had reached 9.87%. This figure is much better than the 6.92% achieved at the end of September but is quite far from the full year growth target (14%) set at the beginning of the year.

That "banks must cure the problem of excess money" was the challenge faced by the banking system in 2023 when granting credit to the economy was still difficult. The main reason is that businesses cannot absorb capital and do not want to borrow, according to Deputy Governor Dao Minh Tu.

Most recently, in order to promote credit into the economy, in December, the Prime Minister had a working session with leaders of 38 commercial banks and many relevant ministries and departments to find ways to open up capital flows. Not only the banking industry, many relevant ministries, agencies, businesses and people are also called upon to unite to achieve the set goals.

Previously, the State Bank also allowed banks to proactively adjust credit room when meeting prescribed conditions such as: reducing lending interest rates, achieving 80% of credit room currently available, or focusing on lending to priority areas.

At the end of the year, deposit interest rates at banks have reached a record low, with interest rates at many terms lower than during the COVID-19 epidemic.

Recently, the giant Vietcombank has decided to reduce short-term deposit interest rates. In particular, if people deposit less than three months, the interest rate will be 1.9%/year, the lowest level in history. Interest rates for terms under 6 months at foreign banks decreased to 2.8%/year, 50 basis points lower than in 2021.

Up to now, 12-month term deposit interest rates have dropped to the lowest level in the past 5 years, ranging from 4.78% to 5.29%/year, lower than the period during the COVID-19 epidemic.

The trend of reducing deposit interest rates at banks has taken place since the end of February when the operator went against the world interest rate trend, reducing operating interest rates four times in a row.

According to data from the State Bank, the average deposit and lending interest rates of new transactions in VND decreased by about 2.0 percentage points compared to the end of 2022.

Although deposit interest rates have decreased quite rapidly, lending interest rates have not decreased commensurately. Explaining this problem, leaders of many banks said that although deposit interest rates decreased sharply, the bank's capital costs did not decrease as quickly because there were still high-interest-rate deposits from the end of the previous year, so reducing loan interest requires a certain delay.

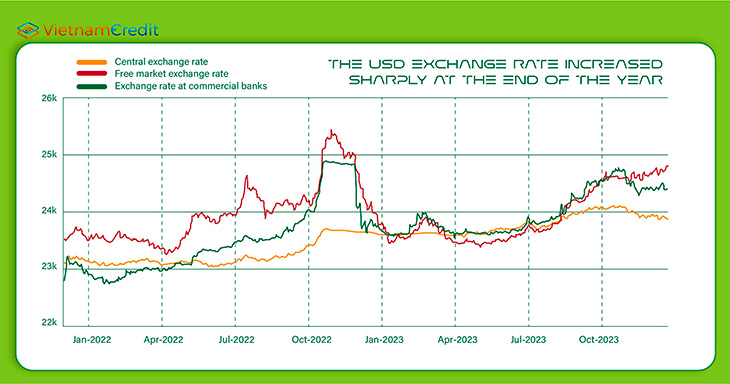

The strengthening of the USD in the international market has created great pressure on the currencies of other countries around the world, including VND.

The USD exchange rate has recorded a period of strong fluctuations since the end of August, the selling price of USD at some banks at times exceeded the threshold of 24,600 VND/USD. The depreciation rate of the Dong as of the end of September exceeded 3%. The central exchange rate also exceeded the 24,000 VND mark for the first time and peaked at 24,110 VND on October 23.

In the last month of the year, the exchange rate cooled somewhat, the depreciation of VND compared to USD was estimated to be about 2.6% by SSI Research (December 20).

Latest update on December 26, Vietcombank's listed exchange rate closed around 24,040 - 24,410 VND/USD while the exchange rate on the free market fluctuated in a narrow range, at 24,700 - 24,750 VND/USD. The central exchange rate was 23,870 VND/USD.

Exchange rate developments in the third quarter are somewhat similar to the end of the previous year when the domestic exchange rate fell sharply after increases in previous months, with the trigger coming from the international environment helping cool down sentiment in the market.

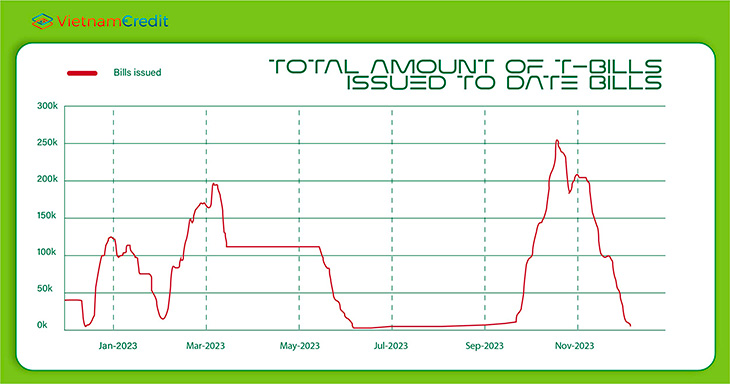

After about 15 weeks of no transactions on the open market, on September 21, the State Bank restarted the money-sucking channel by issuing Treasury bills (T-bills). Around 10,000 billion VND was net withdrawn on the first day and the operator extended this channel until November 8.

According to experts, the move to issue T-bills can help adjust liquidity in the system, push up interbank interest rates and help reduce the difference in interest rates between USD and VND, thereby reducing exchange rate pressure in the domestic market in the short-term.

Explaining this move, Deputy Governor of the State Bank of Vietnam Pham Thanh Ha shared that the State Bank must regulate short-term bills to reduce excess liquidity in the system, trying not to have a major impact on the interest rate level.

Many economic experts believe that the State Bank's move to sell T-bills is a normal activity of central banks and does not mean a reversal of monetary policy.

The SBV chose to issue T-bills as a plan starting in 2023, instead of selling foreign exchange reserves like in 2022, to limit the long-term impact on the liquidity of the banking system. The main purpose of the State Bank is to absorb liquidity in the market 2 to reduce pressure on short-term exchange rate speculation.

As of December 6, all batches of bills issued in the previous period have matured. The current amount of treasury bills is 0.

In 2023, banks will no longer make money as easily as in previous years when facing low credit demand, high credit costs and increased risks of bad debt. Bank profits have shown a decreasing trend compared to the same period last year.

In the third quarter, the after-tax profit of the entire banking industry reached more than 47,892 billion VND, down 1.2% over the same period. The rate of profit decline has cooled compared to the previous quarter. In particular, the group of state-owned commercial banks (Big4) is the only group that recorded positive growth (up 7.2% over the same period). The profits of the other commercial banks decreased by 5.2%. Banks with the strongest decrease include PG Bank, VietABank, VietBank, ABBank.

The increase in non-performing loans is not too surprising to the market in the current difficult economic context. This was also previously predicted by operators and experts. That the economy recovered slowly, businesses encountered difficulties, combined with the freezing of the real estate and corporate bond markets has continued to reflect the bank's bad debt situation.

The amount of non-performing loans of the entire industry has increased for the fourth consecutive quarter since Circular 14 related to COVID-19 debt restructuring expired, increasing to 2.2%. However, the increase is tending to slow down in the third quarter of 2023.

The implementation of Circular 02 has created conditions for banks to keep customers' debt groups intact, contributing to restraining the increase of bad debt. According to the State Bank of Vietnam, by the end of September 2023, the total outstanding debt restructured according to Circular 02 reached 140,000 billion VND (accounting for 1.09% of total credit in the whole system).

The positive point about the quality of banks’ assets in the third quarter of 2023 is that group 2 outstanding loans decreased by 7.7% compared to the previous quarter. Analysts believe that banks’ asset quality will be temporarily controlled until the end of 2023. However, the problem of bad debt will have to be paid more attention next year.

Source: SBV, Wichart, vietnambiz

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")