2023 is also the year when a number of large banks in the US and Switzerland fell into collapse and bankruptcy. Four regional banks in the US including: Silicon Valley Bank, Signature Bank, First Republic Bank and Silvergate Bank have collapsed or liquidated their assets. On the other side of the Atlantic, Credit Suisse - Switzerland's second largest bank - had to sell itself to a rival.

These fluctuations have had a very negative impact on the risk situation in financial and banking markets around the world and of course have spillover effects to Vietnam.

Following are the three main risks in the financial market of Vietnam.

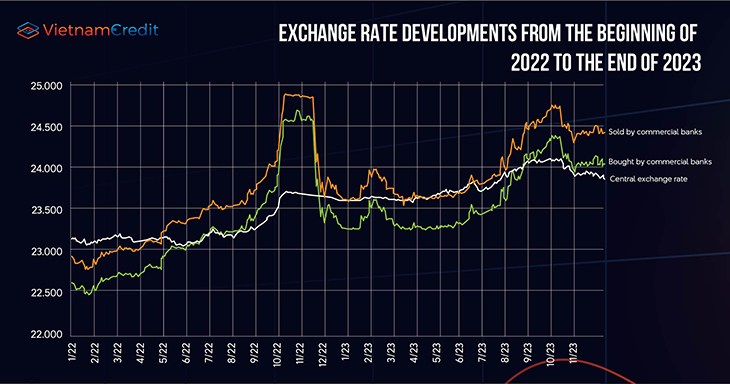

This risk still exists and always exists. However, exchange rate pressure in 2024 has eased. In 2023, the USD decreased in value by about 2.23%, the previous year it increased by nearly 8%. Clearly, exchange rate pressure has gradually eased from the third quarter of 2023. After that, Vietnam's exchange rate had a few months of fluctuations but for the whole year, it only increased by 2.6% and remained under control.

For 2024, the pressure is much less thanks to three main reasons. Specifically, this year, there will not be much exchange rate pressure because the Fed will not raise interest rates anymore, which means the USD will decrease in value. Not to mention the worsening US economy is also the reason why the USD depreciates.

At the same time, the balance of payments is basically quite stable, last year it was positive by several billion USD and it is forecast to continue to be positive this year. The trade balance in 2023 has just recorded a record surplus, FDI capital and remittances into Vietnam are still good, helping Vietnam's balance of payments forecast to be slightly positive.

Along with that, the supply and demand relationship of foreign currency related to borrowing and payment is guaranteed. Therefore, it is forecast that in 2024, the exchange rate will increase at 1-2%.

In 2024, imports turnover may recover but at most they will only grow equal to export turnover, the trade balance is still quite balanced.

The main service export is tourism. It is expected that international tourism will be better than 2023.

The only thing is that if the global situation is unstable and inflation remains high, central banks may slow down the monetary easing process in 2024. As a result, pressure on exchange rates and interest rates for Vietnam will not small.

In recent years, bad debt has increased but is still under control. Especially if we separate the bad debts of weak banks, including SCB, the current on-balance sheet bad debt level of the Vietnamese banking system is about 3%, meeting the requirements of Resolution 01 of the Government. According to this Resolution, the banking system's on-balance sheet bad debt must be below 3%, and gross bad debt must be below 5%.

It is believed that this year, the State Bank of Vietnam (SBV) can still control bad debt risks. With Circular 02, the SBV has been considering and may extend this circular if necessary (the immediate deadline of this Circular is June 30). If it is not extended, it will be more difficult to access credit for businesses and borrowers, and bad debt will increase. However, it should not be too long, and should not be extended too long because otherwise it will raise risks.

Risks are still there and create a sense of dependence on borrowers, so there must be a time limit to end this. However, according to Dr. Can Van Luc, it should be extended until the end of this year to reduce difficulties and challenges.

Interconnection of the corporate bond, banking and real estate markets

The interconnection of the corporate bond, banking and real estate markets is also a major risk. Basically, this risk has been identified and especially related to cross-ownership which is being controlled quite strongly, not allowing the risk to spread. In particular, the SCB incident that occurred late last year was also controlled. On the one hand, the financial system is more sustainable and the experience in handling risks is also better.

Dr. Can Van Luc, BIDV Chief Economist and Director of BIDV Training and Research Institute, Member of the National Financial and Monetary Policy Advisory Council.

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")