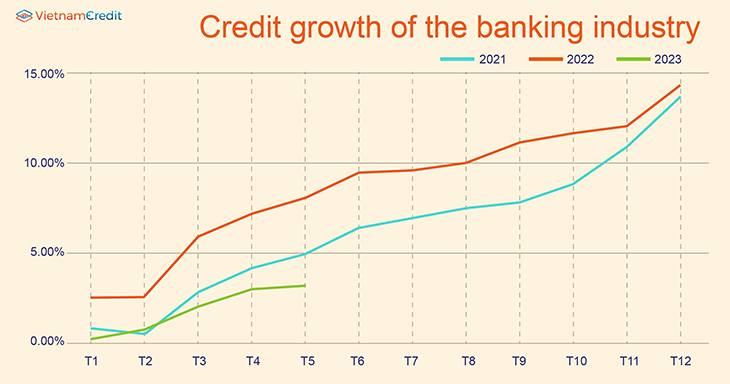

In the first half of the year, the most mentioned issue was that credit growth was very slow, much lower than the same period in previous years. According to the State Bank of Vietnam (SBV), by the end of June 2023, the economy's outstanding debt reached more than VND 12.4 million billion, an increase of 4.73% compared to 2022 while the figure for the same period last year increased by more than 8.5%.

Credit growth slows due to slowing economy, weak real estate market, slowing down production activities due to weakness from main export markets as well as high interest rates reducing credit demand.

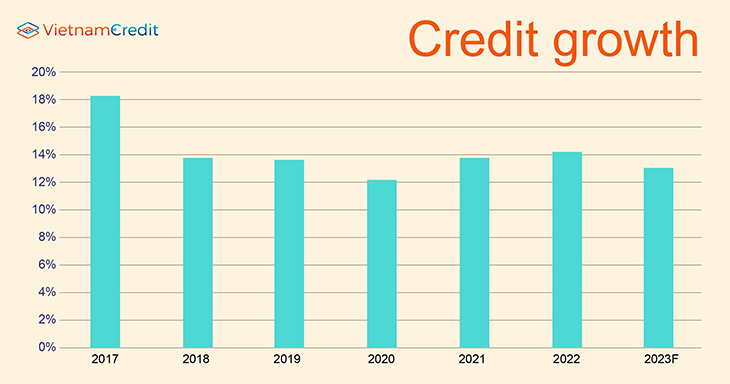

The level of deposit interest rates is decreasing quite rapidly and is expected to gradually reduce lending rates. Along with that, the economy may recover better in the second half of 2023. Many securities companies forecast that credit growth in 2023 will be lower than last year, ranging from 11% - 12.5%, Bao Viet Securities (BVSC) is more optimistic with an expectation of 13%.

Since the beginning of the year, the State Bank has reduced the operating interest rate 4 times in a row, causing the deposit rate to drop rapidly from the peak in early 2023.

The average deposit interest rate of commercial banks has decreased by about 0.7%/year compared to the end of 2022, currently at 5.8%/year; average lending interest rate in VND decreased by 1%/year at about 8.9%/year.

Deposit interest rates of banks cooled down rapidly along with slow credit growth, which slowed down the demand for deposits as banks had high deposit growth in the fourth quarter of 2022.

"With the SBV's orientation to reduce interest rates to support the economy as well as slow growth of credit demand, deposit rates may decrease further in the second half of the year, but the rate of interest rate reduction will slow down.", BVSC commented.

Data from the General Statistics Office also shows that the difference between credit and capital mobilization has narrowed significantly to only about VND 92,000 billion, from nearly VND 300,000 billion at the end of April.

In the interbank market, liquidity did not face much pressure, the overnight interbank interest rate even fell to 0.39%, the lowest level since March 2021. As of the end of June, interbank interest rates for terms ranged from 0.7% to 3.1%, down more than 4 percentage points compared to the end of 2022.

The rapid increase in deposit interest rate from the fourth quarter of 2022 has resulted in a rapid increase in the cost of capital while the lending interest rate has been adjusted more slowly (every 3-6 months), leading to a faster increase in capital costs than interest rates, reducing NIM of banks in the first quarter.

The reduction of the operating interest rate 4 times in the first half of the year will help banks stabilize again and may increase slightly in the second half of 2023.

The high interest rate in the fourth quarter of 2022 also made people and businesses improve their cash flow management as well as increase the use of available money to limit borrowing. Since then, the CASA ratio of banks has declined, especially in the first quarter of 2023. Techcombank lost its CASA position and MB rose to the top.

According to analysts of BVSC, in the short term, the CASA ratio is under pressure, but when interest rates decrease further, the downward pressure on CASA will gradually lift. Besides, the speed of digital transformation of banks is taking place strongly as well as the promotion of not using cash from the Government and the State Bank, CASA will increase again in the long term.

In the first 6 months of the year, the dong (VND) was stable in the context of the SBV continuously cutting operating interest rates. The USD/VND exchange rate was relatively stable and rebounded at the end of the second quarter.

The exchange rate on the interbank market inched up in May 2023 (up 0.13% compared to April), and in June alone it increased by 0.4% compared to the end of May. In the informal market, the free rate rose 0.8% in June.

Analysts believe that the VND will continue to suffer from devaluation pressure in the second half of 2023 as the USD - VND interest rate gap continues to widen. Data from VDSC shows that the USD-VND interest rate differential in the interbank market is at a record high, the highest is 4.4 percentage points for the overnight interest rate and the lowest is 0.6 percentage point for the 3-month term interest rate.

Pressure on VND remains when the Fed expects to continue raising interest rates and seasonal pressure comes from FDI enterprises' profit repatriation. The positive point comes from the disbursed FDI inflows remaining quite well (reaching USD 10 billion in the first 6 months - equivalent to the same period) or the large surplus of trade balance (estimated more than USD 12 billion in the first 6 months) due to a decrease in imports.

Currently, banks have not announced business results and financial statements for the second quarter, so there are no data on profits and changes in bad debts of banks.

However, according to the business trend survey conducted by the State Bank recently, credit institutions said that the business situation of the banking system in the second quarter continued to "improve" significantly slower than the previous quarter. Their pre-tax profit grew slightly but lower than expected in the previous survey period

According to the assessment of credit institutions, the ratio of bad debt to credit balance of the banking system showed a "slight increase" in the second quarter of 2023 but is expected to decrease in the third quarter of 2023.

Credit institutions forecast that customers' demand for banking services will grow positively in the third quarter of 2023 but at a slower rate in 2023 compared to 2022.

Capital mobilization of the whole system of credit institutions is expected to increase by an average of 3.2% in the third quarter of 2023 and by 10.6% in 2023. Credit balance of the banking system is expected to increase by 4.4% in the third quarter of 2023 and increase by 12.5% in 2023.

Source: vietnambiz

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")