At the end of October, several banks continued to announce the auction of bad debts such as factories, hotels, buildings, etc., all of which are assets worth tens to hundreds of billions VND. In such context, preliminary updates on business results of the third quarter reporting season also showed initial information about growing bad debt concerns.

In the case of Kien Long Bank, the NPL ratio (group 3 to group 5) increased from 1.9% to 2.14% at the end of the third quarter of 2023 according to the third quarter consolidated financial report. This is still much lower than the general level of 3%, but it should be noted that the slow decrease was due to the increase in credit scale, but the total NPLs has increased by 21% in value.

Another worrying thing is that interest and fees receivable also increased by nearly 50% in the first 9 months of the year, which mainly came from credit activities (up more than 54%) despite the fact that interest income for loans also increased (more than 62%).

Another case is Vietcombank, when subprime debt increased rapidly according to a new report. The NPL ratio of this bank increased from 0.68% at the end of 2022 to 1.21%, of which total bad debt increased by 84%.

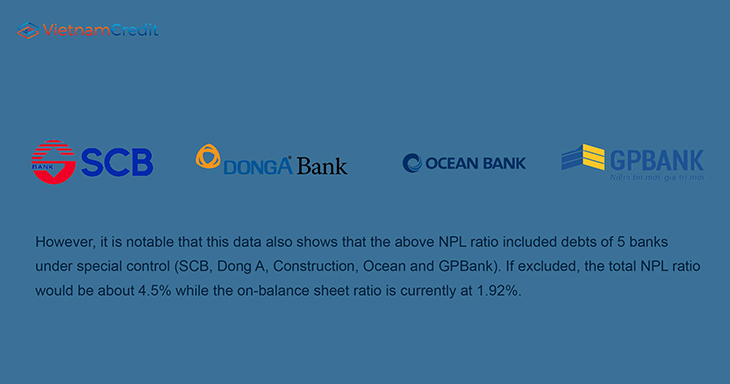

According to a recently published report to the National Assembly, data from the State Bank shows that the system's on-balance sheet NPLs tend to increase rapidly from 2022 and continued this trend in the first months of 2023. By the end of July, the on-balance sheet NPL ratio was about 3.56%, a sharp increase compared to 2% at the beginning of the year. The "full" NPL ratio (including amounts kept in the same group, corporate bonds with potential bad debt, bad receivables, accrued interest that must be withdrawn, etc.) was up to 6.16%.

However, it is notable that this data also shows that the above NPL ratio included debts of 5 banks under special control (SCB, Dong A, Construction, Ocean and GPBank). If excluded, the total NPL ratio would be about 4.5% while the on-balance sheet ratio is currently at 1.92%.

Previously, data for the first 6 months of the year showed that the NPL ratio of the 25 largest listed banks increased to 2.1% at the end of the second quarter of 2023, from 1.9% at the end of the first quarter. Data at that time also showed that the total value of debt restructuring according to Circular 02 of the State Bank of Vietnam issued in 2023 was about VND 62,500 billion, equivalent to 0.5% of the total credit of the whole system.

Concern about increased bad debt is a common for all banks. According to the results of the Business Trends survey for the fourth quarter of 2023 with all credit institutions, the general assessment shows that the NPL ratio in the third quarter increased slightly, but is expected to decrease slightly in the last quarter of this year.

The overall risk level of customer groups is believed to continue to increase slightly in the third and fourth quarters, but the growth rate may slow down compared to the previous quarter. However, this year’s risk level has increased significantly compared to last year, but is expected to decrease slightly next year. Data show that about 63% of credit institutions assess the overall risk of customer groups at a "normal" level, while 32.4% assess it at a high or quite high level.

In recent announcements about preliminary business results for the third quarter, most banks focused on the story of revenue and profits facing difficulties due to the general market situation, but rarely mentioned the bad debt issue.

In Techcombank's report, the bank informed that its asset quality continues to be under control and is in line with the third quarter 2023 forecast on the formation of debt that needs attention and bad debt. The bank's NPL ratio is at 1.4% (1.3% if combined with loans and corporate bonds).

In terms of policy, there are currently many important regulations that directly support bad debt. One is Circular 02 allowing debt repayment term structure and keeping the debt group intact until the end of the first half of 2024 to reduce pressure on both banks and borrowers. The second policy that has been mentioned a lot recently is debt rollover. Another one is the legalization of Resolution 42 of the National Assembly on bad debt handling, which will expire at the end of this year.

However, some of these policies are considered by experts to not be fully effective and in line with management expectations. In reality, the number of loans restructured is not much because not all customers meet the conditions. Similarly, many banks said that customers are not interested in reversing their debt because of the complicated procedures and do not want it recorded in their credit history.

Regarding this policy, in a recent conference organized by the State Bank of Vietnam on October 27, General Secretary of the Banking Association Nguyen Quoc Hung said that from the perspective of banks, there are also problems related to the Circular 02 on debt structure, so it is necessary to remove and adjust appropriately so that credit institutions have more resources to share difficulties with businesses and the economy during difficult times.

Currently, although interest rates are low compared to the beginning of the year and banks also want to disburse funds, not everyone wants to borrow due to the decline in international demand and the domestic market.

Therefore, most experts assess that the recovery of the market is the most important factor. In the context of the economy reducing leverage but rapidly increasing bad debt, banks will still face many difficulties if orders do not return promptly.

Current concerns mostly lie in real estate assets and corporate bond debt. According to calculations by Maybank IB Vietnam Securities Company at the beginning of the year, in a bad scenario, about 30-40% of bond and real estate debt will be converted into bad debt, thereby increasing the bad debt ratio by about 4%.

However, according to MSVN's assessment, the overall health of the Vietnamese banking system as well as other macro factors (national credit rating, economic growth, interest rate level) is much stronger than in 2012, the period of economic crisis due to frozen real estate.

Source: thesaigontimes

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")