In a recent report on the banking industry, KB Securities Vietnam (KBSV) forecasts that in the last months of 2023 and in early 2024, the net interest margin (NIM) of state-owned banks and ACB will improve more slowly than the entire industry due to its role in "supporting the economy".

KBSV assesses that capital cost pressure remains when high-interest-rate deposits with 1-year terms will not mature until late 2023 or early 2024. Banks will need another one to two quarters to bring the cost of finances (COF) to a level similar to developments in operating interest rates.

In addition, deposit interest rates have now reached the bottom like during the COVID period, leaving little room for further reduction. KBSV noted the risk that increasing deposit interest rates will hinder the speed of improving capital costs. Some banks have increased deposit interest rates again to increase the proportion of long-term deposits, meet Circular 06 and prepare sources for credit growth at the end of the year.

Regarding lending interest rate, analysts found that the interest earning assets (IEA) of banks in the monitoring list continued to decrease by 17 basis points (bps) in the third quarter of 2023 compared to previous quarter. In particular, the state-owned banking group and some large commercial joint stock banks such as ACB and STB have had a decrease of 20 - 30 bps due to customer support policies.

KBSV estimates that in the coming time, IEA will maintain a downward trend as banks compete with lending interest rates to solve the credit growth problem and the loan portfolio structure shifts from individual customer groups to corporate customers, which have lower interest.

KBSV believes that banks' NIM in the fourth quarter of 2023 will recover more slowly than expected, and even tend to decrease. By 2024, low interest rates will be fully reflected in capital costs while lending interest rates decrease slowly and with a delay. On that basis, the banking industry's NIM in 2024 will improve more clearly, but cannot return to the high level of 2022.

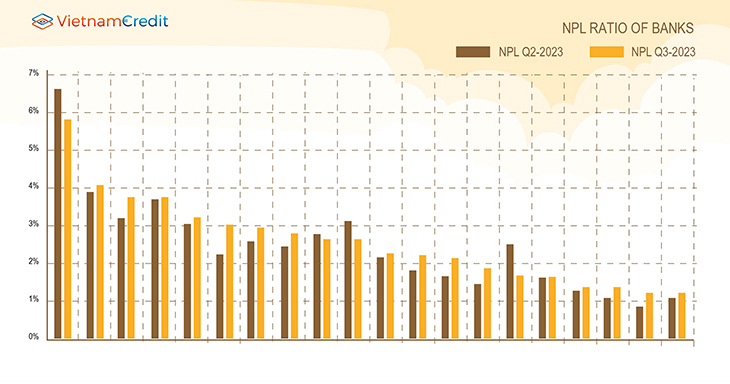

According to KBSV statistics, the increase in bad debt or non-performing loans (NPL) tended to slow down in the third quarter of 2023. The implementation of Circular 02 has created conditions for banks to keep customers' debt groups intact, contributing to restraining the increase of bad debt.

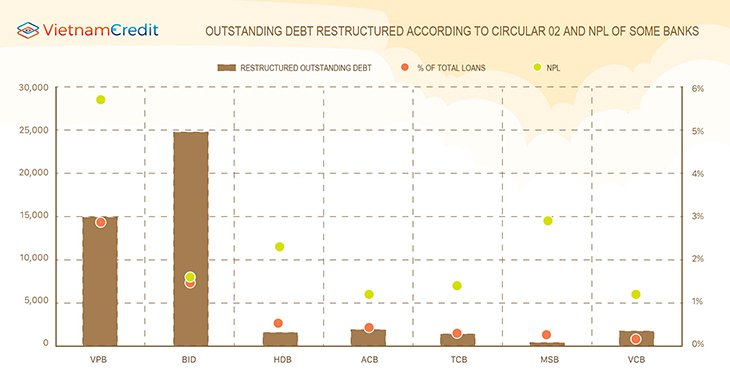

According to the State Bank, as of the end of September 2023, the total outstanding debt restructured according to Circular 02 reached VND 140,000 billion (accounting for 1.09% of total credit in the whole system). KBSV information shows that VPBank has a structured debt of VND 14,900 billion (accounting for 2.86% of outstanding debt), and BIDV has nearly VND 20,000 billion (about 1.5% of outstanding debt).

For the remaining banks, because the pressure on bad debt is not too great and they do not prioritize using Circular 02 (due to having to make more provisions), the restructured debt accounts for a small proportion of the total outstanding debt. Of which, Vietcombank's restructuring rate reached 0.14%, ACB reached 0.4%, Techcombank reached 0.27%, MSB reached 0.25% and HDBank reached 0.5%.

According to KBSV's assessment, the positive point about banks’ asset quality in the third quarter of 2023 is that group 2 outstanding debt decreased by 7.7% compared to the previous quarter. Analysts believe that asset quality of banks will be temporarily controlled until the end of 2023. However, the problem of bad debt will have to be paid more attention next year.

KBSV believes that the risks making bad debt swell in 2024 may come from Circular 02 expiring in June 2024, causing debts to be restructured into the correct classification group. In addition, banks' reserve buffers will shrink in 2023, leaving little room for processing.

It is believed that banks with diverse customer files, adequate provisioning, solid reserve buffers, and little exposure to real estate and corporate bonds will be able to control credit risk costs better than other banks.

On the contrary, banking groups with low coverage ratios (below 50%) will be under a lot of pressure and have no room to remove bad debt from the balance sheet.

After three quarters of modest growth in net interest income (NII), KBSV estimates that in the fourth quarter of 2024, this item of banks will record more positive results when credit accelerates in the last months of the year.

Non-interest income of banks in 2023 has encountered difficulties due to developments in the bond and insurance markets. According to KBSV, banks will need more time to bring non-interest income back to last year’s growth level.

Analysts point out that investment banking operations depend on the recovery level of the corporate bond market and investor confidence. This field is expected to return in 2024, but it will be difficult to increase as strongly as during the boom period of 2019 - 2021. Insurance premium growth will gradually recover as banks and insurance companies improve service quality and protect the interests of customers.

According to KBSV, the basic outlook for credit growth in 2024 is 13 - 14%, with operating costs continuing to be controlled but high credit cost pressure will dominate pre-tax profits.

Experts predict that pre-tax profit growth of banks in the monitoring list will reach 10% next year. This list includes 10 banks: Vietcombank, BIDV, VietinBank, ACB, Techcombank, MB, Sacombank, VPBank, TPBank and MSB.

Source: KBSV

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")