Although lending interest rates have begun to decrease and banks have continuously launched incentive programs and reduced interest rates, outstanding credit balances still increase very slowly, and may even decrease. Credit growth among banks has had a clear differentiation since the beginning of the year.

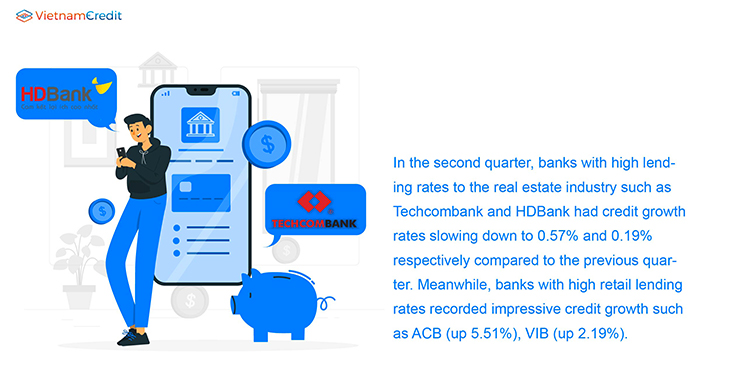

In the second quarter, banks with high lending rates to the real estate industry such as Techcombank and HDBank had credit growth rates slowing down to 0.57% and 0.19% respectively compared to the previous quarter. Meanwhile, banks with high retail lending rates recorded impressive credit growth such as ACB (up 5.51%), VIB (up 2.19%).

The two banks with the highest credit room (about 24%) also had high credit growth in the second quarter - MB increased by 6.49% and VPBank increased by 5% compared to the previous quarter.

Recently, sharing at the Bank-Enterprise Connection Conference in Bac Ninh province, Ms. Nguyen Thi Quynh Giao - Deputy General Director of BIDV, said as of September 26, 2023 the bank's credit growth reached 7%, higher than the industry average, however in some areas such as Bac Ninh, outstanding debt only increased by 1.7%.

A representative of VietinBank shared that the bank has recorded positive credit growth compared to the general market level, but is still far from the plan.

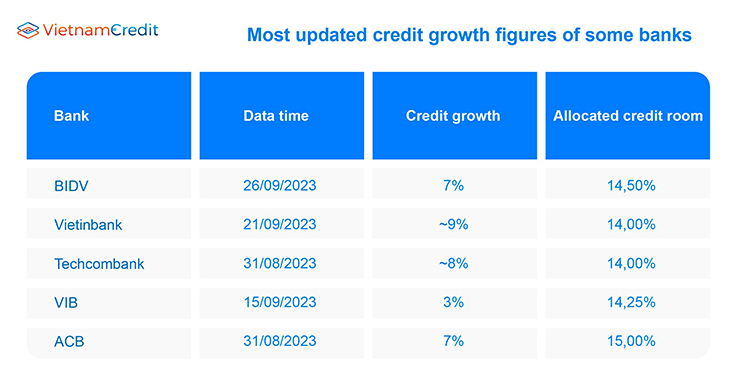

Most updated credit growth figures of some banks

Although the credit growth figure for the entire banking system has not been disclosed, Mr. Nguyen Thanh Tung, General Director of Vietcombank, said that in Hanoi, where many large corporate and state-owned enterprise customers are located, Vietcombank's credit still decreased by 2.2%.

In addition, the real estate business and real estate consumer lending (a segment accounting for 70% of the bank) also decreased sharply due to market fluctuations. Real estate lending to individual customers in Hanoi decreased by 15% while the growth of corporate customers could not compensate for the decline from individual customers.

Mr. Phan Thanh Son - Deputy General Director of Techcombank also said that by the end of August, the bank had achieved credit growth of nearly 11% and will try to achieve the growth target granted by the State Bank from now until the end of the year.

Mr. Son said that interest rates are not the key issue causing low credit growth, but the risks from the business environment and other factors that affect investment decision making. Since the beginning of the year, Techcombank has reduced interest rates 4 times both for new and old customers, with a total outstanding loan balance of VND 21,000 billion.

Techcombank Deputy General Director expects that the combination of monetary policy and fiscal policy will support economic growth in the last months of the year, thereby positively affecting credit demand.

According to Rong Viet Securities (VDSC), ACB said that credit growth had improved to 7% at the end of August, expected to increase by 1-1.5% each month. Credit growth for the whole year is expected at 12 - 14%.

VIB shared that its credit growth had reached 3%, an improvement compared to 0.9% at the end of June. Growth was led by the retail banking sector with products such as real estate loans and business loans while loans for autos are slowing down. Credit growth for the whole year is expected to be 10 - 12%, lower than the allocated room of 14.25%.

The preferential interest rate for loans to buy real estate for the first year at VIB is fixed at about 9.5%/year, a sharp decrease compared to the lending interest rate at the beginning of the year (floating about 16 - 17%/year).

The bank said that to promote credit growth, in addition to the attractive loan policy for purchasing liquidated secured assets, VIB will raise the ceiling on loan value that business units can approve themselves to boost sales activities.

VDSC estimates that VIB's credit growth will reach approximately 12% thanks to a better recovery in credit demand in the context of sharply reduced lending interest rates and led by home loan products.

Source: VDSC, vietnambiz

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")