In every economy (regardless of the sizes), financial transactions are always faced with the possibility of credit risks from many different causes, however, there is often a common consequence that financial obligations when due cannot be fulfilled or only partially fulfilled. These risks cannot be completely eliminated, they can only be limited and preventive. There are many measures to limit credit risk, of which credit rating is one of the common measures aimed at supporting decision-making and management.

In the world, the financial risk assessment and credit rating (CR) have been widely applied by developed countries and conducted by prestigious social organizations.

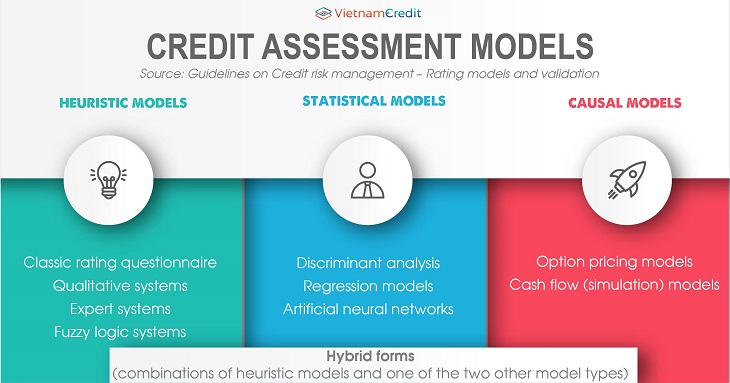

Each credit rating agency uses a distinct rating model to evaluate and rank companies based on the selected input information. Gleaned from the experience of pioneer countries on credit rating around the world, it can be divided into the following rating models:

Source: Guidelines on Credit risk management – Rating models and validation

Each credit rating model has a separate rating process, which clearly shows the characteristics of each model. However, the general steps can be summarized as follows:

Step 1: Determine the content and criteria to be assessed.

Step 2: Determine the score chart corresponding to each norm.

Step 3: On the basis of the established symbol and indicator system, analyze data and information about the enterprise to give points for each indicator.

Step 4: Summarize the score and credit rating of the business.

Step 5: Make comments on the strengths and weaknesses of the business, and at the same time make the recommendations and proposals necessary in accordance with the evaluation objectives.

With this model, the objective judgments about the current financial situation of the business and forecast about its future development are made from the available experience of experts. Criteria to be assessed are business lines, geographic location, financial status, debt relationship of enterprises with banks and other financial institutions, etc. Based on the experience of experts, the answers which show a high risk of bankruptcy must be assigned a greater score than those with a low risk of bankruptcy. This ensures the consistency and practicality of the model.

The statistical model aims to verify statistical hypotheses based on empirical data. In the credit rating process, the use of statistical models requires the creation of hypotheses related to the probability of business bankruptcy. Two statistical models commonly used in practice are the discriminant analysis model and the regression model. Financial indicators using historical data to assess is the characteristics of this credit rating model.

The causal model in the credit rating process is drawn directly from the credit rating analysis on the basis of financial theory, including option pricing model and cash flow model. During the development of these models, statistical methods were not used to test hypotheses for empirical data. With the option pricing model, the likelihood of a company's bankruptcy in the coming year depends on the difference between the asset value and the face value of its debts, and this difference is measured by the standard deviation of the company's asset value.

This is a measure of the distance to bankruptcy, given that the standard deviation of the company's asset value will drop dramatically before the bankruptcy occurs. Cash flow model can be considered as a special case of option pricing model, in which the market value of an enterprise is calculated on the basis of cash flow. This is the difference in the evaluation criteria of this model compared to the heuristic model.

In fact, hybrid forms are widely used by credit rating agencies around the world. Heuristic models can be combined with one of the other two credit rating models (causal models and statistical models). This approach brings many advantages thanks to the addition of advantages between the methods. For example, the advantages of a statistical and causal model lie in being more objective and capable of classifying than heuristic models. However, statistical and causal models can only be used to assess certain factors related to creditworthiness.

Without the knowledge of credit rating experts, important information about the object being rated may not be included in the evaluation process. In addition, not all statistical models have the ability to process qualitative information directly (such as discriminant analysis models), or these models may require a large amount of data to ensure the accuracy of the model (for example, logistic regression models). The data is usually not available and is difficult to collect in large amount. Therefore, in order to get a broad and insightful picture of the creditworthiness of companies rated in these cases, it is necessary to use it in combination with the heuristic models to process qualitative data.

>> Credit rating: models and applications (part 2)

References:

1. Investor Bulletin: The ABCs of Credit Ratings [Online]. U.S. Securities and Exchange Commision.

2. NCIF (2017), "The role of corporate credit rating in implementing policies to support Vietnamese SMEs" Henry Tran - VietnamCredit

Henry Tran - VietnamCredit

")

")

")

")

")

")

")

")

")