The year 2020 was more successful than expected in the banking industry, although many other industries and the economy have suffered significant losses because of the COVID-19 pandemic. In the banking systems, most banks recorded growth not only in profits but also in other important business indicators, such as revenue, assets, mobilized capital, credit. The credit quality management was better meanwhile remaining a very low NPL (Non-Performing Loan) ratio.

In terms of profit, the last year witnessed one bank with a profit of USD 1 billion, which was Vietcombank. Additionally, five banks recorded a profit of over VND 10,000 billion, namely VietinBank, Agribank, MB, Techcombank, and VPBank. Some banks had very high growth rates (from 40% or more), including ACB, HDBank, VIB, or even more than double the previous year such as MSB.

Also, Vietnam's foreign exchange reserve by the end of 2020 was estimated at USD 100 billion. The increase in total assets of credit institutions as of October 31, 2020, was 4.75% compared to the end of 2019,...

However, the year 2021 is forecasted to cause more difficulties to the banking industry due to the delayed impact of the COVID-19 pandemic in the past year. Furthermore, the pandemic wave has come back, significantly impacting other sectors, thereby affecting banks. On the global scale, S&P Global Ratings warns that 2021 will be the toughest year for banks since the global financial crisis. The biggest risks of the banking industry include the possibility of having a more negative credit rating, declined government support, an increase in insolvency, and a weakening real estate market.

Domestically, the difficulties of banks that can be easily seen are the potential risk of bad debts (after restructuring debt maturities, waiving or lower interest rates for customers affected by the COVID-19 pandemic according to Circular 01). This risk may increase this year when Circular 01 terminates. The actual profits tend to decrease due to increased risk provision, plus interest rate cuts to support businesses.

However, besides the shared difficulties, many banks are still considered to have certain advantages over the rest.

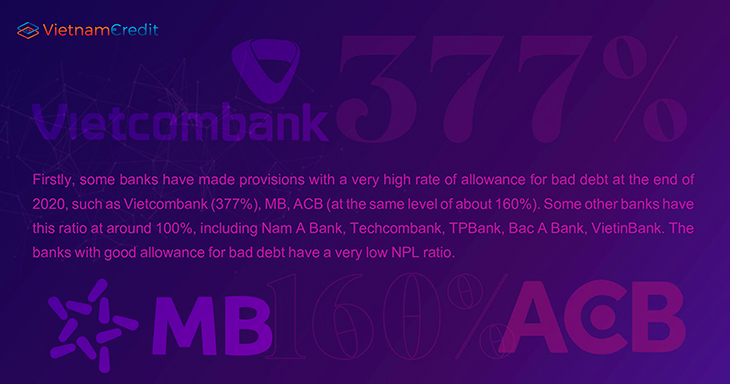

Firstly, some banks have made provisions with a very high rate of allowance for bad debt at the end of 2020, such as Vietcombank (377%), MB, ACB (at the same level of about 160%). Some other banks have this ratio at around 100%, including Nam A Bank, Techcombank, TPBank, Bac A Bank, VietinBank. The banks with good allowance for bad debt have a very low NPL ratio.

In the coming time, even after the termination of Circular 01, these banks do not have to worry too much about the bad debt burden, even profits can be added up through the reversal of provisions.

Secondly, banks that have the retail sector, cross-selling service, especially bancassurance, will also have advantages this year, for example, Vietcombank, VIB, ACB, VietinBank, MB, Techcombank, and Sacombank.

Thirdly, banks with a thriving digital segment will have advantages because they can easily deploy products and services on digital platforms and attract more customers, who are becoming more and more familiar with digital products and utilities. Currently, banks with successful digital transformation recently are VPBank, VIB, HDBank, TPBank, MB, Viet Capital Bank, Vietcombank, OCB, etc.

Besides, banks with strong foundations, good risk management, high reputation, high standards of the State Bank of Vietnam (SBV), and international standards will also have an advantage in joint development. Some banks in this aspect are Vietcombank, HDBank, VIB, MSB, MB, etc.

Compiled by VietnamCredit

")

")

")

")

")

")

")

")

")

")