Electronic components industry is a supporting industry, providing intermediate inputs including semiconductors and electronic application components for assembly and manufacture of final electronic products.

In Vietnam, the industry has begun to be formed and developed along with Vietnam’s electronics industry since the mid-70s. Within 20 years since 1990, Vietnam’s electronic components industry had experienced robust transformation and development. The compound annual growth rate of the industry from 1990 to 2010 ranged between 20% and 30%. Noticeably, during the period 1995-2000, the electronic components industry witnessed a significant growth of 30-45% per year.

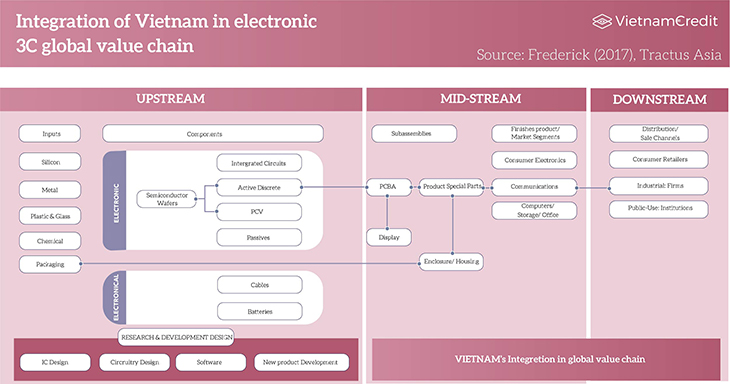

Vietnam started to engage intensely in the global electronic 3C value chain since 2010 as a centre for electronic component assembly. However, the integration of Vietnam into the 3C global value chain remains weak, especially in the upstream segment, as the activities of domestic enterprises are mostly at low value-added. Besides, due to the heavy reliance on imports of sophisticated components, Vietnam’s domestic companies have difficulties participating in the supply chain of foreign invested companies.

Source: Frederick (2017), Tractus Asia

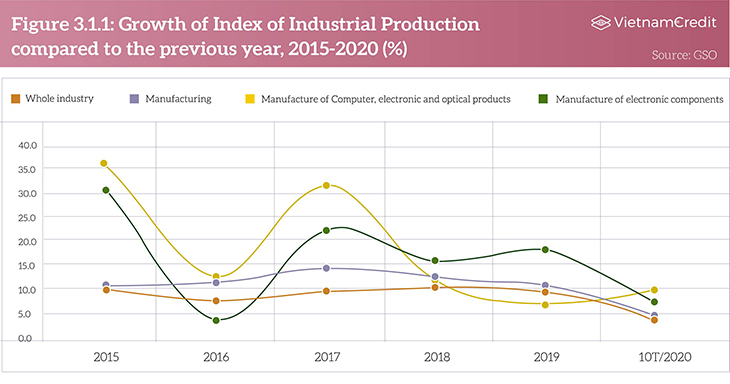

Except for 2016, the Index of Industrial Production (IIP) growth rate of electronic components manufacturing sector remained higher than that of the manufacturing industry and the whole industry within five years since 2015. From 2017 to 2019, electronic components industry has witnessed a stable growth of IIP, ranging between 15% and over 20%.

Source: GSO

Since the second quarter of 2020, the electronic components producing sector started to be affected by the Covid-19 pandemic due to the decrease of customer demand in key markets, the disruption of supplying sources and the delay or cancellation of import-export orders. IIP of electronic components industry in the first 10 months of 2020 grew slightly, estimated at 6.8% over the same period last year.

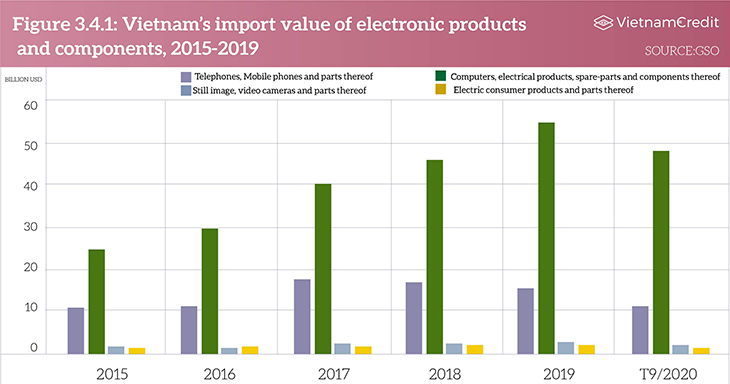

Vietnam’s imports of electronic products and components have experienced a positive growth in the past 5 years in terms of turnover. The value of imported of electronic products and components rose from 36.7 billion USD in 2015 to 70.5 billion USD in 2019. Of which, the value of the group of computers, electrical products, spare-parts and components thereof accounted for the largest proportion of the total, reaching over 70% each year.

In the first 9 months of 2020, the total import turnover of electronics and components reached 59 billion USD. Of which, computers, electronic products and components contributed more than 45 billion USD.

Source: GDVC

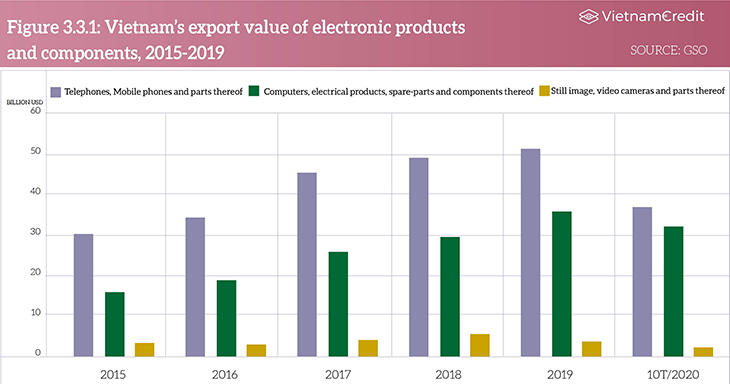

Vietnam’s exports of major electronic products and components witnessed an increasing trend in value, growing from 48.8 billion USD in 2015 to approximately 100 billion USD in 2019. Although the group of telephones, computers, electrical products, cameras and their components in Vietnam posted a trade surplus of approximately 30 billion USD in 2019, the sector of computers, electrical products, spare-parts and components thereof experienced a trade deficit of around 17 billion USD in same year.

Source: GDVC

China is the largest telephones, mobile phones and parts trading partner of Vietnam, accounting for nearly 52% of total import value. Korea is the second largest supplier with more than 40% of the import turnover. Some other major markets exporting large value of electronic components to Vietnam are Hong Kong and Japan. In terms of consumption, the United States, China, South Korea and the EU markets are the key customers of Vietnam's electronics industry.

Regarding the group of electronic products, computers and components, Korea, China, Taiwan, the United States, and Japan are Vietnam’s main suppliers. In which, Korea hold a leading position in providing electronic products, computers and components with nearly 34% of the total turnover. China ranked second with nearly 24% of the total, followed by Taiwan, the United States and Japan with the contribution of 10.8%, 9.5% and 8.7%, respectively. China and the United States are the two largest consumption markets for this group of products, followed by Hong Kong, Korea, Taiwan, and the EU.

Vietnam’s electronic components industry currently experienced an imbalance between imports for trading and manufacturing since the import tax for electronic components is lower than that of materials to produce components. Therefore, domestic enterprises with lack of capital and cutting-edged technology will prefer trading imported complex components over producing components themselves. The heavy reliance on foreign investment, production and export is a great pressure for the industry. Besides, this also leads to the weak participation of local businesses in the 3C global value chain as well as the FDI companies’ supply chain.

Since Vietnam has been successfully contained the coronavirus, the country is on track for GDP expansion, especially in the manufacturing sector of electronic components. Besides, many suppliers are diverting their production from China to Vietnam, bringing more opportunities for domestic enterprises.

Although being impacted by the Covid-19 pandemic, the electronic components manufacturing industry has been remaining a positive growth rate, demonstrating its great potential of recovery and development. Besides, with the initiatives of the Vietnamese government to support the electronic components industry, domestic enterprises are expected to have progress in production in the upcoming time.

VietnamCredit

")

")

")

")

")

")

")

")

")

")