In the last article regarding due diligence, we have given you details about the preventable causes for failure in due diligence. By identifying these causes, we could come up with a set of helpful principles assisting buyers in increasing the chances of success. These principles could be derived from the preventable causes in the last article as follow:

With a comprehensive look at the whole transaction and scientific predictions, the M&A group will have identified chances and reduce their risks.

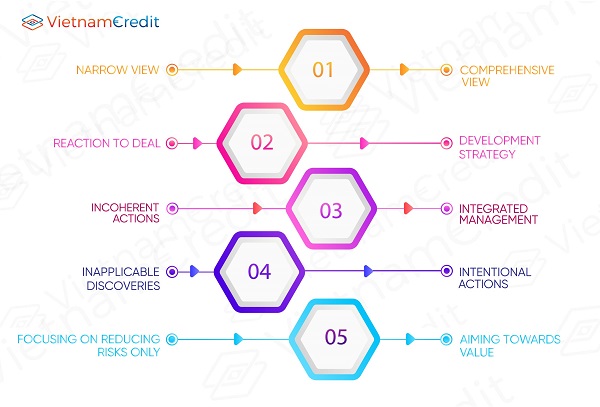

In our point ò view, the scale of due diligence should be wide enough to identify and locate all the risks and opportunities existing in the transaction. We use the term “comprehensive due diligence” in discussions to emphasize this. Especially, comprehensive due diligence must go with a suitable development strategy, must provide decisions regarding acquisition, trade terms, and structure, as well as the directions of the acquiring company prior to and post-transaction.

Following an M&A deal should be considered a development step in the suitable general development strategy planned out by the company. This process will help the company in gathering agreements on the strategy to occupy a specific part of the market, and furthermore, it will help in setting the list of potential acquiring objectives that are suitable to the strategy, easing the target approaching process. This process also provides the due diligence group with a set of important variables and assumptions that need to be checked during the inspection.

Information coordination, communication, and sharing scientifically play crucial parts in the management of the due diligence activities. The key to effectively manage a group consisting of different elements is the distribution of the due diligence goals in a top-down form, based on the opportunities and risks of each transaction.

The challenges facing the due diligence group do not lie solely in the key role of the decision about whether to follow through with the deal or not. Their missions are much more difficult, including the task of answering the question: What should the company minimize risks and fully exploit the opportunities which create value for the shareholders?

This viewpoint plays a directive role in performing due diligence. Instead of being dominated by information provided by the sellers, the due diligence group should set up their own clear goals and actively try to fulfill them. Moreover, due diligence can not end as soon as the due diligence report regarding the observed statistics is created. Its missions are to turn those “seemingly soulless” numbers into practical actions that will be carried out by the M&A prior to and post-transaction, including negotiation and transaction activities reform, planning and post-acquisition consolidation deployment, etc.

In order to make sure that a transaction will result in the desired results in both the acquisition and profits dimension, the due diligence process must focus on both the task of reducing risks and maximizing the value. The due diligence group should approach this process with the mindset of both an investor and an auditor, while simultaneously using the objectives of creating value as the compass leading the majority of the actions of the group.

As mentioned in the last article, there are some preventable causes leading to failure in making a due diligence report, and if you want to be profitable, you must take actions and make adjustments to help turn those causes into your advantages

>> Due Diligence Reports

")

")

")

")

")

")

")

")

")

")