On November 29, 2019, the Governor of the State Bank signed Decision No. 2497 / QD-NHNN on the interest rates of compulsory reserve deposits and deposits in excess of compulsory reserves of credit institutions at the State Bank of Vietnam. This decision takes effect on December 1, 2019.

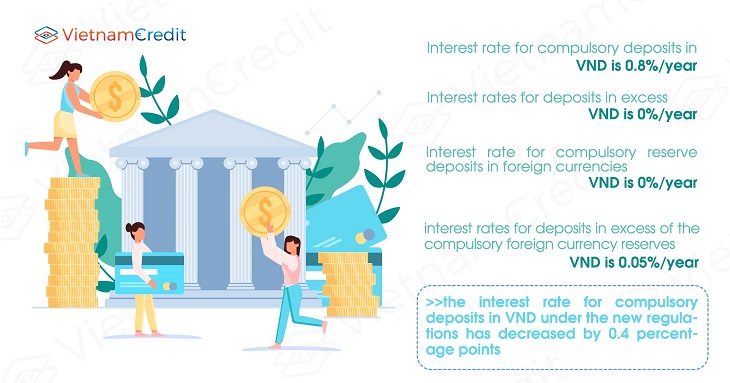

Specifically, the interest rate for compulsory deposits in VND is 0.8%/year, interest rates for deposits in excess of VND reserves are 0%/year; The interest rate for compulsory reserve deposits in foreign currencies is 0% per annum, the interest rates for deposits in excess of the compulsory foreign currency reserves are 0.05% per year.

Thus, compared with the rate of 1.2% per year under Decision 1716 / QD-NHNN in 2005, the interest rate for compulsory deposits in VND under the new regulations has decreased by 0.4 percentage points. Meanwhile, the deposit interest rate in excess of the obligatory reserve remained unchanged.

Talking to us, Mr. Nguyen Duc Do - banking and finance expert said that reducing the compulsory reserve interest rate (DTBB) will make commercial banks gain less interest from deposits at the State Bank. The impact of reducing the reserve interest rate is not large, only when the deposit interest rate exceeds the reserve requirement is encouraged, banks will be encouraged to use the money to lend to the economy instead of over-deposit rates in SBV.

Commenting on the recent loosening actions of the State Bank of Vietnam, this expert said that the overarching objective of the regulator is still to reduce lending rates for businesses. It is not out of the question, economic growth is slower and needs more support from credit flows.

Meanwhile, BVSC's analysis team thinks that reducing interest rates paid for basic loan accounts also helps the SBV save a certain cost in the policy management process.

Moreover, in the world, Japan and Europe are the regions that are applying negative interest rates (-0.1% and -0.5% respectively) for commercial banks' deposits at the central bank when over a certain threshold. This means that commercial banks even have to pay a fee to the central bank instead of enjoying interest.

Reducing interest rates for compulsory deposits and exceeding compulsory reserves encouraged banks with excess liquidity, regularly having deposits exceeding the compulsory reserve levels at the SBV to increase lending activities to the economy instead of leaving money with the SBV to enjoy interest rates.

"It is likely that the credit growth situation in the first 11 months of the year is quite far away from the target of 14%, so the SBV is strengthening solutions to boost credit. This move is also "in sync" with a series of recent monetary policies related to reducing the ceiling interest rates and lending to priority areas, reducing OMO lending interest rates, reducing credit interest rates” - said BVSC.

")

")

")

")

")

")

")

")

")

")