It is clear that understanding how to work with company financial reports is an important task for many corporations and firms. The idea of analysis and interpretation based on a balance sheet, business performance report and cash flow statement can

It is clear that understanding how to work with company financial reports is an important task for many corporations and firms. The idea of analysis and interpretation based on a balance sheet, business performance report and cash flow statement can reveal the health of a company becomes completely popular, as it used to teach in some subjects at universities. However, company financial report is always complicated with a wide range of numbers and indices, so many people think it is too difficult for them to comprehend. In this article, I will draw your attention to some typical characteristics that we are required to clearly understand before focusing on the financial issues of any company.

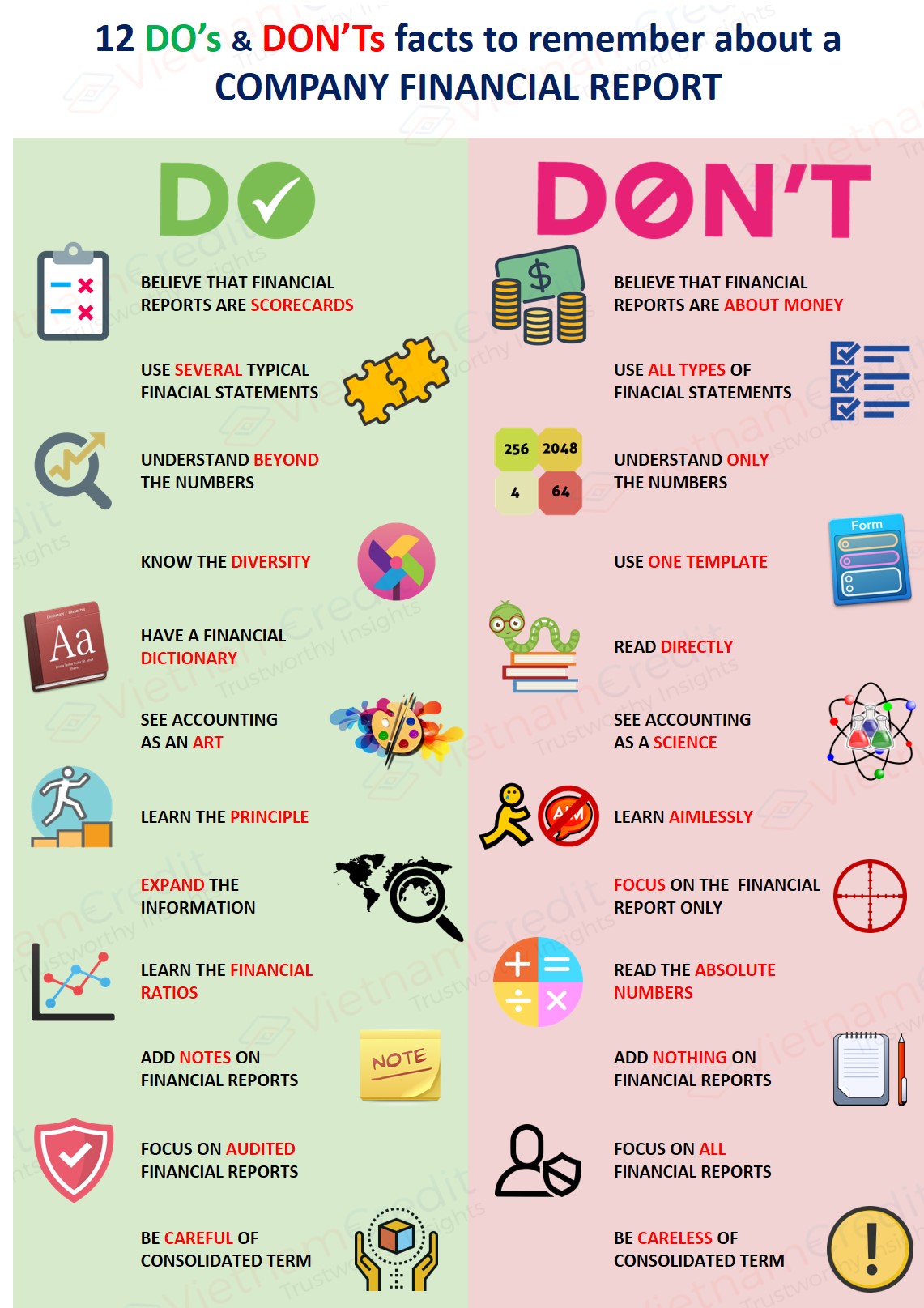

1. FINANCIAL REPORTS ARE SCORECARDS.

There are millions of investors, including individuals and organizations in the world. While many investors choose mutual funds to invest, there are many others who invest directly in company stocks. In order to invest prudently, it requires them to look for profitable companies with good balance sheets, sustainable revenue, and positive cash flow. Whether you are able to analyze yourself or ask for advice from experts, learning the basic financial analysis skills is totally useful. Entrepreneur Robert Hollet has written a book called “How to score in Business (1987)”. He made the point that in business, companies use the money to show its scores, and the scoreboard is the financial report. He realized that "many people do not understand how to score in business." They often get confused ".

Similarly, most investors often make the mistake, especially when it comes to the ability to evaluate the possible profit through financial statements. But of course, we can avoid that mistake. As Michael C. Thomsett wrote in Mastering Fundamental Analysis (1998):

"There is nothing called “top secret” on Wall Street or in any industry. In the financial world, you may rarely face too complex situations. The basic principles, as the name implies, are basic and relatively simple. The only thing that complicated financial information is that the terminology, statistical analyzes and mathematical formulas that we cannot simply discuss through a conversation."

2. WHICH FINANCIAL STATEMENTS SHOULD WE USE?

For investment analysis purposes, you should use a balance sheet, a statement of income and a statement of cash flows. Shareholder equity and retained earnings are occasionally offered but those are not the important information used by financial analysts. Sometimes, there is a situation where many investors focus only on business results and balance sheets while they ignore using the cash flow. This is extremely wrong because the cash flow statement plays a crucial role and cannot be underestimated.

3. UNDERSTANDING BEYOND THE NUMBERS

The figures in a company's financial statements reflect real-world events. These numbers and ratios from the investment analysis will be easier to understand if you visualize the actual facts hidden behind this quantitative information. For example, before you start pondering those numbers, you should learn about the company's business, its products, services, and where it operates.

4. DIVERSITY IN THE METHOD OF FINANCIAL STATEMENT PREPARATION

You should not expect that financial statements have only one template. Many articles and books focus on a rigid approach to different financial situations, as a result, inexperienced investors will misunderstand if a report is not "typical" in their own view. Obviously, the diversity of business leads to the diversity of financial reports which vary the types of the balance sheet, while revenue statements and cash flow statements are usually intact.

5. CHALLENGES IN UNDERSTANDING FINANCIAL TERMS

The lack of standardized financial terms makes it difficult to comprehend accounting entries. Some investors are usually confused when they read a financial report. But this problem will not be dangerous in the future, because they can learn all the new terms through a financial dictionary.

6. ACCOUNTING IS AN ART, NOT A SCIENTIFIC

The financial performance ratios of a company, which used to be described in the financial statements, is impacted by the estimates and judgments of the team of managers. Normally, this team can be honest and sincere, and independent auditors can be truthful, strict and cannot be compromised. But in some case, when the auditors were undisciplined, the financial report could be wrong. Therefore, you should believe that auditors and accountants are artists and their performances are the numbers and indices, its accuracy depends on how they abide by the rules.

7. TWO MAJOR PRINCIPLES OF ACCOUNTING

There are many generally accepted accounting principles (GAAP) are used to prepare financial statements. For investors, the principle of historical cost convention and accrual concept are two basic principles to acknowledge. Under GAAP, the asset is recorded at the time of acquisition (historical cost or historical price), although this price may differ significantly from the current price on the market. Revenue is recorded when the goods and services are provided and the cost is recorded when incurred. In general, this value stream does not coincide with the actual cash flow of the business and this isolation makes cash flow becomes extremely important.

8. INFORMATION WHICH IS NOT INCLUDED IN THE FINANCIAL STATEMENTS

Information on the economic situation, industry prospects, level of competition, market dynamics, technology innovation, quality of management and labor force are not reflected directly in the financial statements. Investors need to know that even information from financial reports is important, it is just one piece in the broader picture of investment.

9. FINANCIAL RATIOS

Absolute numbers in financial statements are not valuable in investment analysis. Therefore, to evaluate the performance and financial position of a company, investors need to convert them into relative ratios. These ratios and indicators have to be considered for a long time to reflect all the tendencies. The concept of using those figures can vary considerably depending on the industry, size, and stage of development of the company.

10. NOTES TO THE FINANCIAL STATEMENTS

It is difficult for regulatory authorities to understand the figures that the financial statements show them. Professional analysts agree that adding notes to the financial statement presentation is necessary for the evaluation of the company's financial performance. As auditors often write in the financial statements, "the accompanying notes are an integral part of the financial statements."

11. AUDITED FINANCIAL STATEMENTS

Wise investors should only focus on investing in companies that have audited financial statements, and this is also a requirement for all public companies. Therefore, before analyzing the financial statements of a company, you must read the auditor's report. An objective view will influence your decision to keep going or stop investing. The opinion of the audit may be good or bad, but in any case, you can manage the risk according to those ideas.

12. CONSOLIDATED FINANCIAL STATEMENTS

In general, the term "consolidated" sometimes appears in the name of a financial statement, as in the consolidated balance sheet. The merger of a parent company and a subsidy means that the operation of individual entities is combined as an economic unit. This custom leads to the fact that the merging statement of the entire entity is more important than that of the individual entities and investors should pay attention to this issue.

>> Financial report: Definition and significance

")

")

")

")

")

")

")

")

")

")